Printable F10 North Dakota Template

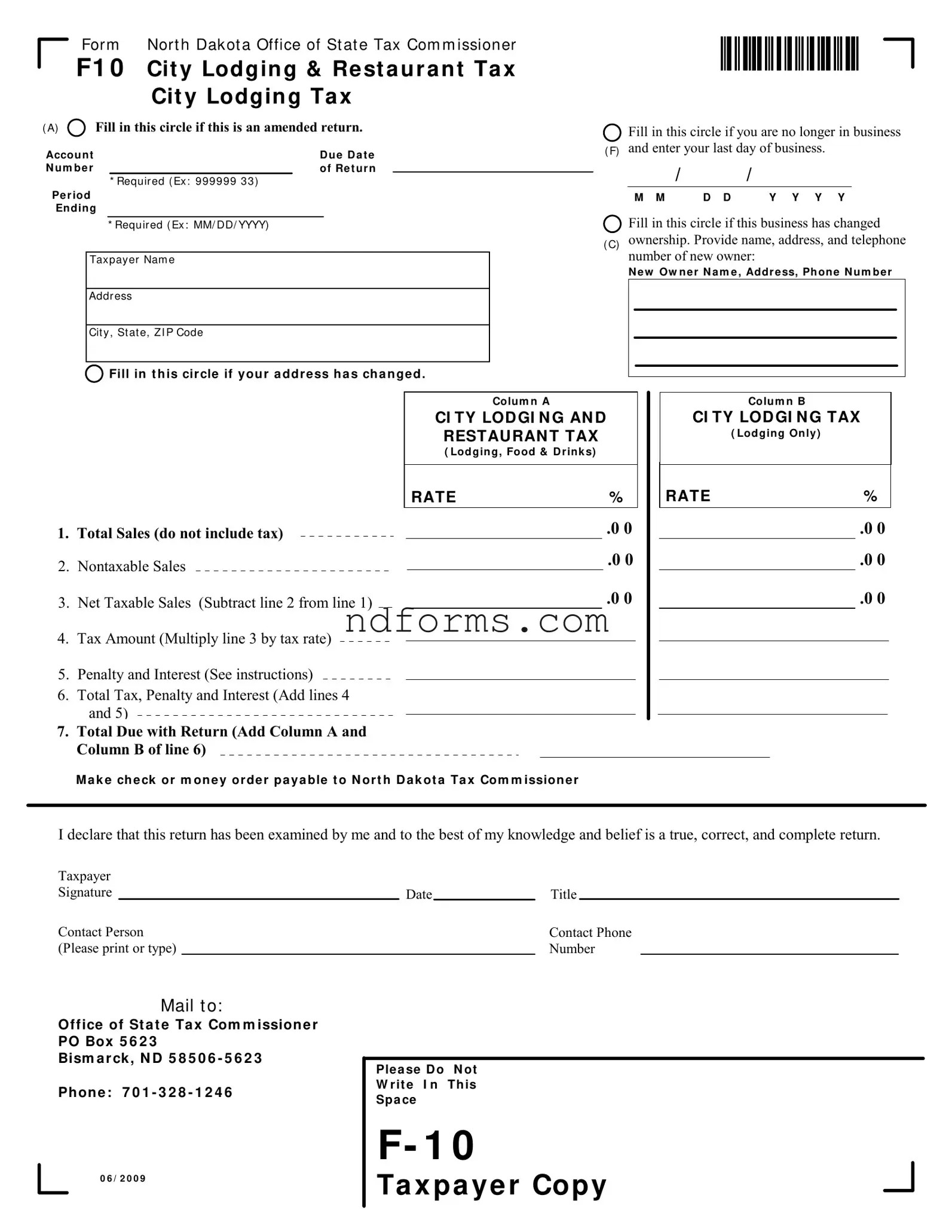

The F10 North Dakota form is a crucial document managed by the Office of State Tax Commissioner, specifically designed for businesses providing lodging and restaurant services within the state. This form enables businesses to report and remit the taxes that apply to lodging and dining, ensuring compliance with local tax laws. The layout of the form captures essential information, such the period of the tax return, business identification details, and operations specifics such as whether the business is new, has changed ownership, or is closing down. It breaks down sales into total, nontaxable, and net taxable sales across two main categories: city lodging and restaurant tax, and city lodging tax only. The form helps calculate the tax amount due based on the net taxable sales, and includes sections for reporting penalty and interest in case of late filing or payment, leading to a total amount due with the return. Detailed instructions accompany each section to guide taxpayers on how to accurately fill out the form, making the process as straightforward as possible. Making a mistake on this form can have financial implications, such as additional penalties and interest for late or incorrect filings. Hence, it is more than a document; it is a compliance tool that facilitates the smooth running of businesses engaged in hospitality services in North Dakota.

Form Preview

For m Nor t h Dak ot a Office of St at e Tax Com m issioner

F1 0 Cit y Lodgin g & Re st a u r a n t Ta x Cit y Lodgin g Ta x

( A)  Fill in this circle if this is an amended return.

Fill in this circle if this is an amended return.

Accou nt |

|

|

D u e D a t e |

|

N u m b e r |

|

|

of Re t ur n |

|

|

* Requir ed ( Ex : 9 999 99 3 3) |

|||

Pe r iod |

|

|

|

|

End ing |

|

|

|

|

*Requ ir ed ( Ex : MM/ DD/ YYYY)

Tax pay er Nam e

Addr ess

Cit y , St at e, Z I P Code

Fill in this circle if you are no longer in business ( F) and enter your last day of business.

/ |

|

/ |

M M |

D D |

Y Y Y Y |

Fill in this circle if this business has changed

Fill in this circle if this business has changed

( C) ownership. Provide name, address, and telephone number of new owner:

N e w Ow n e r N a m e , Addr e ss, Ph on e N u m be r

Fill in t h is cir cle if y ou r a dd r e ss h a s ch a n ge d .

1.Total Sales (do not include tax)

2.Nontaxable Sales

3.Net Taxable Sales (Subtract line 2 from line 1)

4.Tax Amount (Multiply line 3 by tax rate)

5.Penalty and Interest (See instructions)

6.Total Tax, Penalty and Interest (Add lines 4 and 5)

7.Total Due with Return (Add Column A and Column B of line 6)

Colum n A

CI TY LOD GI N G AN D RESTAURAN T TAX

( Lodgin g, Food & D r ink s)

RATE |

% |

.0 0

.0 0

.0 0

Colu m n B

CI TY LOD GI N G TAX

( Lod ging On ly )

RATE |

% |

.0 0

.0 0

.0 0

M a k e ch e ck or m on e y or de r p a y a ble t o N or t h D a k ot a Ta x Com m ission e r

I declare that this return has been examined by me and to the best of my knowledge and belief is a true, correct, and complete return.

Taxpayer |

|

|

|

|

|

||

Signature |

|

|

Date |

|

Title |

|

|

Contact Person |

|

|

Contact Phone |

Revised 07/01/2002 |

|||

(Please print or type) |

|

|

|

Number |

|||

|

|

|

|

||||

Mail t o:

Of f ice of St a t e Ta x Com m ission e r PO Box 5 6 2 3

Bism a r ck , N D 5 8 5 0 6 - 5 6 2 3

Ph on e : 7 0 1 - 3 2 8 - 1 2 4 6

0 6 / 2 0 0 9

Ple a se D o N ot

W r it e I n Th is

Spa ce

F- 1 0

Ta x pa y e r Copy

Instructions

Line 1 – Total Sales. Enter on line 1, your gross sales for the period including lodging receipts, bar and lounge receipts, restaurant receipts, and all other sales and service charges for the period. This figure should not include any tax collections.

Line 2 - Nontaxable Sales. Enter all sales included in line 1 that are not subject to tax. Nontaxable sales include:

•In Column A and Column B: all sales exempt from North Dakota sales tax including sales to exempt entities, sales of nontaxable service, sales for resale, sales delivered outside of state. Also include bad debts originally reported as a taxable sale with the tax remitted, but written off during this period as uncollectible.

•In Column A: sales subject to state sales tax but not subject to city lodging and restaurant tax. The imposition of city lodging and restaurant taxes varies from city to city. Please contact the Office of State Tax Commissioner if you need additional information.

•In Column B: sales subject to state sales tax but not subject to city lodging tax. City lodging tax applies only to the gross receipts from leasing or renting hotel, motel, or tourist court accommodations within the city for periods of less than thirty consecutive days or one month. It does not apply to food, alcoholic beverages, phone service, durable goods, etc.

Line 3 - Net Taxable Sales. Subtract line 2 from line 1.

Line 4 – Tax Amount. Multiply line 3 by the tax rates printed in the column headings.

Line 5 – Penalty and Interest. Penalty and interest apply to all returns paid or filed after the due date. Penalty and Interest are calculated separately for Column A and Column B. For the first month the return is late, the penalty is 5 percent of the tax due on line 4 or $5, whichever is greater. For each additional month or fraction of a month the return is late, add an additional penalty of 5 percent of the tax on line 4 up to a maximum of 25 percent. Interest does not apply to the first month a return is late, but applies at a rate of 1 percent each month or fraction of a month the return remains late or unpaid.

Line 6 – Total Tax, Penalty, and Interest. Enter the total of line 4 and line 5.

Line 7 – Total Due with Return. Enter the total of line 6, Column A and Column B.

Make your check payable to North Dakota Tax Commissioner. The taxpayer or taxpayer’s agent must sign the return. Please PRINT the name and phone number of a contact person who can answer questions about this return.

Office of State Tax Commissioner

PO Box 5623

Bismarck, ND

Phone 701.328.1246

www.nd.gov/tax

File Attributes

| Fact | Detail |

|---|---|

| Form Title | F10 North Dakota City Lodging & Restaurant Tax |

| Purpose | For reporting and paying city lodging and restaurant taxes |

| Governing Law | North Dakota state tax law |

| Amended Returns | Option available for amending previously filed returns |

| Business Status Changes | Sections to indicate change of address, ownership, or business closure |

| Tax Calculation | Based on net taxable sales and specific tax rates for lodging and/or restaurant sales |

| Penalty and Interest | Applied to late payments or filings, with a specific calculation method |

| Nontaxable Sales | Guidelines for identifying and deducting nontaxable sales from gross sales |

| Payment Method | Make checks or money orders payable to North Dakota Tax Commissioner |

| Contact Information | Included for further assistance or clarification |

| Submission Details | Form and payment mailed to the Office of State Tax Commissioner |

| Special Instructions | Detailed guidance provided for accurately completing each section of the form |

How to Write F10 North Dakota

Filling out the Form F10 for the North Dakota Office of State Tax Commissioner involves reporting your city lodging and restaurant tax information correctly. The steps below are designed to help you complete this form accurately and ensure compliance with state tax regulations. The process is straightforward if you follow each step carefully, guaranteeing that all the necessary details are provided. Remember, an accurate and complete form submission helps in avoiding any potential penalties or issues that might arise from incorrect information.

- Determine if you need to fill in any of the circles at the top section of the form. If you are amending a return, mark the appropriate circle (A). If your business is no longer operating, mark circle (F) and include the last day of business. If there has been a change in business ownership, mark circle (C) and provide the new owner's details. Similarly, mark the circle if your business address has changed, and update your information accordingly.

- Enter your Account Number and Period Ending date in the required fields. Your account number is unique to your business, and the period ending date should reflect the last day of the reporting period.

- Provide Taxpayer Name and Address information, including the city, state, and ZIP code.

- Calculate your Total Sales and enter the amount in line 1. This includes all gross sales but should not include tax.

- In line 2, enter all Nontaxable Sales. These sales are not subject to tax and can include various exemptions as outlined in the form's instructions.

- Subtract Line 2 from Line 1 to find your Net Taxable Sales and record this amount in line 3.

- Compute the Tax Amount by multiplying the net taxable sales (line 3) by the corresponding tax rate for city lodging and restaurant tax (Column A) and city lodging tax (Column B), then enter these amounts in line 4.

- If applicable, calculate and add Penalty and Interest in line 5. This applies to late or unpaid returns.

- Sum up the Total Tax, Penalty, and Interest for both columns and enter this in line 6.

- Calculate the Total Due with Return by adding up the amounts from Column A and Column B of line 6 and input this in line 7.

- Ensure you make your check or money order payable to North Dakota Tax Commissioner.

- Sign and date the form, and provide the title along with a contact person's name and phone number for any inquiries.

- Mail the completed form and payment to the Office of State Tax Commissioner, using the provided address.

After ensuring all parts of the form are accurately completed, reviewed, and signed, mailing it to the specified address is the final step. Timeliness in submitting this form is crucial to avoid possible penalties. Retaining a copy for your records is recommended. This ensures that you have documentation of your submission and can be helpful in case any questions arise from the Office of State Tax Commissioner. By following these detailed instructions, you can confidently complete and submit your Form F10, maintaining compliance with North Dakota's tax requirements.

Your Questions, Answered

What is the F10 North Dakota form used for?

The F10 North Dakota form is specifically designed for businesses to report and pay the city lodging and restaurant tax. It is used for declaring total sales, subtracting nontaxable sales, calculating net taxable sales, determining the tax amount based on applicable rates, and including any penalty and interest if the return is filed or paid after the due date.

Who needs to fill out this form?

Any business that collects sales from lodging, food, and beverages within cities in North Dakota that impose a city lodging and restaurant tax must complete and submit the F10 form. This includes hotels, motels, tourist courts, restaurants, and bars.

How do I calculate the tax owed?

To calculate the tax owed, subtract nontaxable sales from total sales to find the net taxable sales (line 3). Multiply the net taxable sales by the tax rate provided for each column (Column A for city lodging and restaurant tax, Column B for city lodging tax only) to find the tax amount (line 4). If applicable, add penalty and interest (line 5) to the tax amount to obtain the total tax, penalty, and interest due (line 6).

What should I do if my business information changes?

If there are changes to your business, such as address change, ownership transfer, or closure of the business, you must indicate these changes on the F10 form. Fill in the appropriate circle to indicate the change, and if there is a new owner, provide their name, address, and phone number directly on the form.

When is the F10 form due?

The due date for the F10 form is specified in the "Due Date" section of the form. This date is critical as filing or paying after this date can result in penalties and interest charges. The specific due date will depend on the reporting period for which you are filing.

Where do I send the completed F10 form?

The completed F10 form, along with any payment due, must be mailed to the Office of State Tax Commissioner at PO Box 5623, Bismarck, ND 58506-5623. Ensure the form is signed and includes the contact information of a person who can answer questions regarding the return.

Common mistakes

Filling out the F10 form for the North Dakota City Lodging and Restaurant Tax can sometimes be confusing. Here are ten common mistakes people often make when completing this form:

- Not checking the appropriate circle at the top of the form for amended returns, business closure, ownership changes, or address changes. It is crucial to indicate any of these circumstances to ensure the information is updated accordingly.

- Failing to include the Account Number or Period Ending Date, or incorrectly filling out these fields. Both are required and must be accurate for the form to be processed correctly.

- Including tax in the Total Sales figure. The form explicitly asks for gross sales without tax, yet it's common to mistakenly add the tax collected to this figure.

- Omitting or incorrectly calculating Nontaxable Sales. Correctly identifying and subtracting nontaxable sales from total sales is essential to figuring out your Net Taxable Sales accurately.

- Miscalculating the Tax Amount due. This mistake can occur if the incorrect tax rate is applied or if the calculation is simply done incorrectly.

- Forgetting to calculate or incorrectly calculating Penalty and Interest for late submissions. The instructions provide a clear formula for calculating these amounts, which is often overlooked or misunderstood.

- Incorrectly adding the totals in Line 6 when calculating Total Due with Return. Each column must be calculated and reported separately before adding them together.

- Neglecting to sign the form or provide complete contact information, which is necessary for the form to be considered valid.

- Using outdated tax rates or not adhering to the current instructions. Tax rates and regulations may change, and using the most current form and instructions is imperative.

- Forgetting to send the form to the correct address or to include payment. It’s important to double-check the mailing address and ensure that your payment is payable to the correct entity.

These mistakes can often be avoided by carefully reviewing the form instructions and double-checking all entered information before submission. Remember, accuracy is key to ensuring your form is processed smoothly and without delay.

For any questions or clarifications, reaching out to the North Dakota Tax Commissioner's Office directly or consulting with a tax professional is advised. Professional guidance can help avoid errors and ensure compliance with all tax obligations.

Documents used along the form

When handling the F10 North Dakota form, which addresses City Lodging and Restaurant Tax, one often needs to gather and fill out several additional documented forms. These forms are crucial for ensuring compliance with state and local tax laws, and they help businesses in accurately reporting and paying their taxes. Described below are nine commonly used forms and documents that complement the F10 form, each serving a unique purpose in the tax filing and reporting process.

- ND Sales & Use Tax Permit Application: This document is necessary for businesses to legally sell products or services in North Dakota. It is the beginning step to collecting sales tax from customers.

- City Specific Lodging & Restaurant Tax Ordinance: Businesses need this document to understand local tax rates and regulations that apply specifically to their city, as these can differ significantly from state laws.

- Employer's Withholding Tax Form: For businesses with employees, this form is used to report and pay state income taxes withheld from employees' wages.

- ND Annual Report Form: Required for corporations and LLCs, this form updates the state on key information about the business, such as addresses and the names of directors or managers.

- Workers Compensation Insurance Documentation: This demonstrates compliance with ND requirements for workers' compensation insurance, vital for businesses with one or more employees.

- Unemployment Insurance Tax Form: Employers use this document to report wages paid to employees and pay the unemployment tax, which funds unemployment benefits in the state.

- Alcoholic Beverage License: Necessary for businesses selling alcoholic beverages, this license ensures that they comply with state regulations concerning the sale of alcohol.

- Food Service License: This assures compliance with health department standards for businesses that prepare and serve food, influencing both safety and tax obligations.

- New Owner Information Form: If a business changes hands, this document provides the state with information about the new owner, which is crucial for tax records and compliance.

Each of these documents plays a critical role in the comprehensive duty of filing and payment of taxes. While the F10 North Dakota form is specific to city lodging and restaurant taxes, these additional forms ensure broader compliance with state and local regulations, covering everything from sales tax collection to employee withholding. Together, they form a framework that supports the smooth and lawful operation of businesses within North Dakota. Understanding and utilizing these documents is essential for navigating the complexities of tax compliance and ensuring that businesses remain in good standing with tax authorities.

Similar forms

The F10 North Dakota form, designed for reporting City Lodging & Restaurant Tax, shares similarities with a range of other tax documents aimed at facilitating the reports of sales and use taxes. These documents, though tailored to their specific jurisdictions or tax niches, encapsulate a format and function reminiscent of the F10 form, adhering to the fundamental requirements of tax reporting—such as identifying taxable and nontaxable sales, calculating taxes due, and detailing penalties and interests for late submissions. Below are a couple of documents that mirror the F10 form in structure and purpose.

Form ST-1, Sales and Use Tax and E911 Surcharge Return: Much like North Dakota's F10 form, the ST-1 form is utilized by businesses to report their sales, calculate due taxes, and distinguish between taxable and nontaxable sales. Both forms require the business to detail total sales, subtract nontaxable sales to find the net taxable sales, and then apply a tax rate to determine the total tax owed. Additionally, they both mandate the declaration of penalties and interest if the submission is late, ensuring compliance through similar structural approaches to tax reporting.

Form UUT-1, Utility Usage Tax Return: This form, while focused on the use of utilities within a certain jurisdiction, parallels the F10 form's structure by asking for total sales or usage, determining the portion subject to tax, and calculating the due tax. The similarity also extends to adjustments for exemptions or nontaxable portions, and the imposition of penalties and interest for late payments. Both forms serve the function of detailing specific tax obligations within their respective domains, with a clear pathway to calculating the taxpayer’s or business’s due contributions to state or local revenues.

Dos and Don'ts

When you're filling out the F10 North Dakota form for City Lodging & Restaurant Tax, it's important to pay attention to details. Here are some dos and don'ts to help ensure you complete the form accurately and comply with tax regulations:

- Do make sure all your business information is up to date. If there have been any changes, such as your address or ownership, indicate these on the form.

- Do carefully calculate your total sales, excluding tax, to ensure you report accurate figures in the designated sections.

- Do subtract nontaxable sales from your total sales to determine your net taxable sales. It's essential to understand what qualifies as nontaxable to avoid mistakes.

- Do multiply your net taxable sales by the correct tax rate provided in the form's column headings to calculate the tax amount owed.

- Don't overlook the penalty and interest section if you're filing or paying after the due date. Penalties are applied differently for each month or fraction of a month that payment is late.

- Don't forget to add the tax, penalty, and interest amounts to determine the total due with your return.

- Don't send your form without ensuring that all necessary signatures are present. The form must be signed by the taxpayer or their agent.

- Don't leave the contact information section blank. Providing a contact person's name and phone number is crucial in case the tax office has questions about your return.

By following these guidelines, you can avoid common mistakes and ensure your tax filing process is smooth and compliant with the North Dakota Office of State Tax Commissioner's requirements.

Misconceptions

When it comes to understanding and filling out the F10 North Dakota form for City Lodging & Restaurant Tax, there are several misconceptions that can lead to confusion and errors. It's essential to clarify these misconceptions to ensure accurate and timely submissions.

Filing is only for large businesses: Any business, regardless of its size, that provides lodging, food, and drinks must file this form if they operate within a city that imposes these taxes.

Only lodging sales are taxable: Both lodging and restaurant (food and drinks) sales are subject to taxation under the F10 form, depending on the city's tax regulations.

Penalties are negotiable: The penalties and interest for late filing are set according to specific rates. These rates are 5 percent of the tax due for the first month late, with an additional 5 percent for each subsequent month, up to a maximum of 25 percent.

All sales are taxable: Not all sales are taxable. Nontaxable sales include sales exempt from North Dakota sales tax, such as sales for resale or sales delivered out of state, among others.

Changes in business details don’t need to be reported: Any changes in business ownership, address, or status (including closure) must be reported using the F10 form.

Interest is waived for the first month: Interest charges do not apply for the first month the return is late, but a 1 percent charge applies every month or fraction thereof afterward.

You can only file after the period ends: Businesses are required to file the F10 form by the due date following the period ending date. Preparation can begin before the end of the period.

The form is complicated: Although it may seem daunting at first, the F10 form contains clear instructions for each line to guide taxpayers through the process.

Electronic submission is unavailable: While this document does not specify, many tax forms, including city lodging and restaurant taxes, can often be submitted electronically through the state's tax website.

Bad debts are non-deductible: Bad debts that were previously reported as taxable sales and had taxes remitted on them can be deducted as nontaxable sales if they are written off as uncollectible during the period.

Carefully reviewing the guidelines and ensuring an understanding of these key points can greatly simplify the process of filing the F10 North Dakota form. When in doubt, contacting the Office of State Tax Commissioner for clarifications is a wise step.

Key takeaways

When it comes to understanding and utilizing the F10 form for lodging and restaurant taxes in North Dakota, there are several key takeaways that businesses need to be aware of. This form is essential for correctly reporting and paying taxes associated with the operation of lodging and restaurant services in the state. Here are the essential points to bear in mind:

- Amendment and Status Changes: The form allows for amendments to a previously filed return. It also has sections to indicate if a business is no longer in operation or if there has been a change in ownership or address.

- Reporting Sales: Businesses must report total sales, specifying amounts that are not subject to tax, to accurately calculate net taxable sales. Not all sales are taxable; understanding which sales are exempt is crucial for accurate reporting.

- Understanding Taxable Sales: The form differentiates between general sales and those specifically attributable to lodging and restaurant services. Knowing which revenues fall into taxable categories is critical for compliance.

- Calculating Taxes: Taxes are calculated by applying specific tax rates to net taxable sales. The form provides separate columns for lodging and restaurant taxes and lodging-only taxes, reflecting different tax rates.

- Penalties and Interest: Late filings or payments attract penalties and interest charges. The form outlines how these charges are calculated, emphasizing the importance of timely submissions.

- Final Amount Due: The form requires the calculation of the total amount due, combining taxes, penalties, and interest for both lodging and restaurant services and lodging only.

- Payment and Submission: Checks or money orders for the amount due should be made payable to the North Dakota Tax Commissioner. It’s essential to ensure that the form is signed by an authorized individual and includes contact information for possible queries.

- Accessing Help: For additional information or clarification, the Office of the State Tax Commissioner is a valuable resource. They can provide specific guidance on how to comply with the state’s tax requirements for lodging and restaurant businesses.

Understanding and adhering to these key points can help businesses correctly report and remit taxes associated with lodging and restaurant services in North Dakota, ensuring compliance and avoiding potential penalties.

Browse Popular Documents

North Dakota Payroll Taxes - Its use is a critical aspect of tax administration in North Dakota, enabling the state to accurately account for income tax withholdings from various sources.

Sfn 847 - By ensuring that all details are correctly filled in, the SFN 847 form minimizes the risks of future disputes.

North Dakota Nonresident Filing Requirements - Accommodates reporting for multiple beneficiaries, ensuring equitable tax handling and distribution of estate or trust income.