Printable Nd 306 Template

In today’s rapidly evolving business landscape, staying compliant with tax obligations is more critical than ever. Among the varied responsibilities that employers in North Dakota face, the obligation to accurately withhold and remit income taxes stands out for its importance and complexity. The Form 306 - Income Tax Withholding Return serves as a crucial tool in this process, designed to simplify the reporting and payment of withheld taxes to the North Dakota Office of State Tax Commissioner. This form, identified by its specific form number (SFN 28229) and the latest revision date (March 2019), is a comprehensive document that accommodates different employer scenarios—including amendments to previous returns, changes in business ownership, and the discontinuation of business operations. Employers are required to detail the total North Dakota income tax withheld during a period, adjustments for amended returns, and compute any applicable penalties or interests due to late submissions. Additionally, the form incorporates sections for ownership information, which is vital in the event of final returns, and detailed instructions for both regular and amended filings. Ensuring accuracy on the Form 306 is essential, not only for adhering to state tax regulations but also for avoiding potential penalties and interest for non-compliance or errors. With provisions for electronic discussions and payments, the form embodies an integration of traditional compliance with modern convenience, simplifying the process for North Dakota employers while reinforcing the importance of precise tax withholding and reporting.

Form Preview

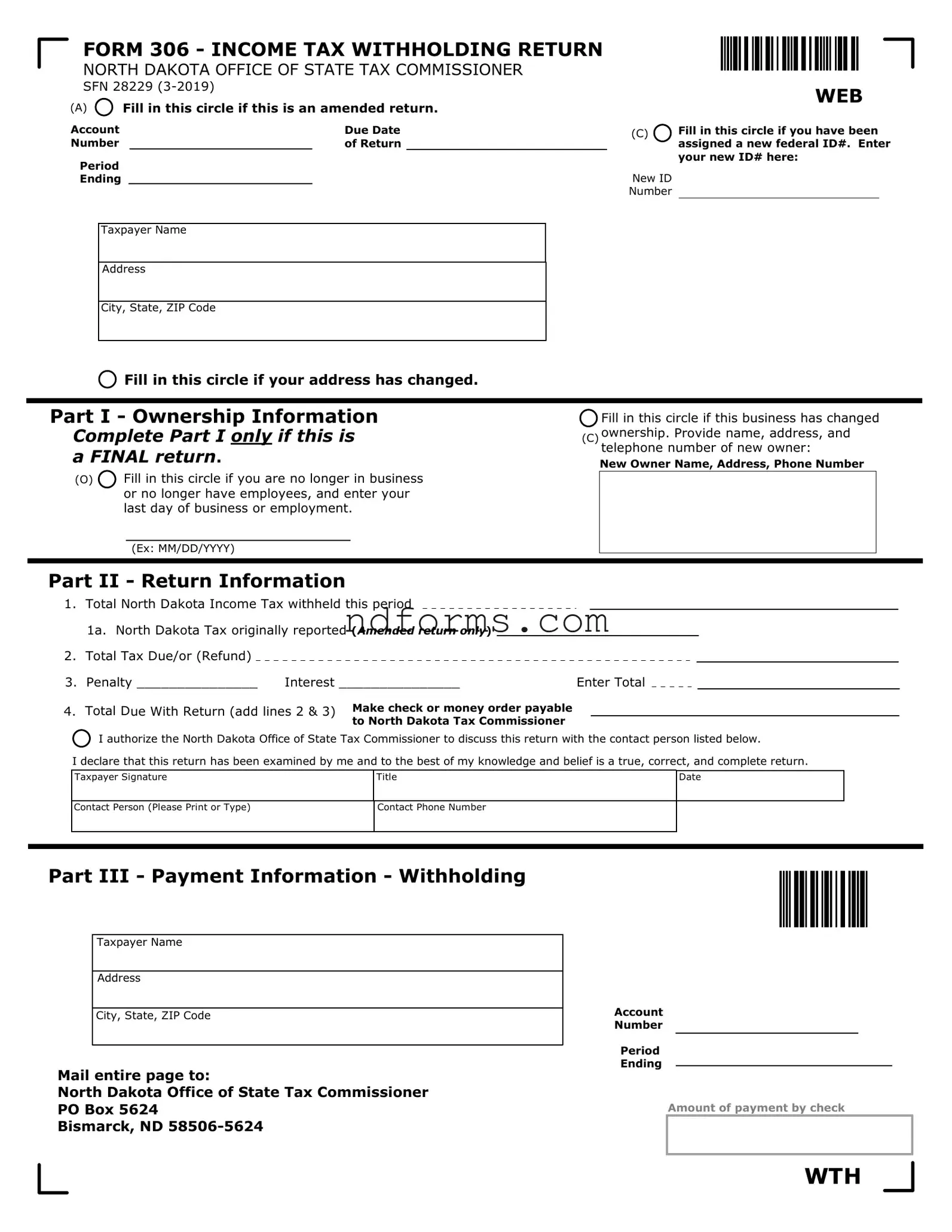

FORM 306 - INCOME TAX WITHHOLDING RETURN

NORTH DAKOTA OFFICE OF STATE TAX COMMISSIONER

SFN 28229

(A) Fill in this circle if this is an amended return.

Fill in this circle if this is an amended return.

Account |

|

Due Date |

|

Number |

|

of Return |

|

Period |

|

|

|

Ending |

|

|

|

Taxpayer Name

Address

City, State, ZIP Code

WEB

(C)Fill in this circle if you have been assigned a new federal ID#. Enter your new ID# here:

New ID

Number

Fill in this circle if your address has changed.

Fill in this circle if your address has changed.

Part I - Ownership Information

Complete Part I only if this is

aFINAL return.

(O) Fill in this circle if you are no longer in business or no longer have employees, and enter your last day of business or employment.

Fill in this circle if you are no longer in business or no longer have employees, and enter your last day of business or employment.

Fill in this circle if this business has changed

(C)ownership. Provide name, address, and telephone number of new owner:

New Owner Name, Address, Phone Number

(Ex: MM/DD/YYYY)

Part II - Return Information

1.Total North Dakota Income Tax withheld this period

1a. North Dakota Tax originally reported (Amended return only)

2.Total Tax Due/or (Refund)

3. |

Penalty _______________ |

Interest _______________ |

Enter Total |

||

4. |

Total Due With Return (add lines 2 & 3) Make check or money order payable |

|

|

|

|

|

|

to North Dakota Tax Commissioner |

|

|

|

I authorize the North Dakota Office of State Tax Commissioner to discuss this return with the contact person listed below.

I authorize the North Dakota Office of State Tax Commissioner to discuss this return with the contact person listed below.

I declare that this return has been examined by me and to the best of my knowledge and belief is a true, correct, and complete return.

Taxpayer Signature

Title

Date

Contact Person (Please Print or Type)

Contact Phone Number

Part III - Payment Information - Withholding

Taxpayer Name

Address

City, State, ZIP Code

Mail entire page to:

North Dakota Office of State Tax Commissioner PO Box 5624

Bismarck, ND

Account

Number

Period

Ending

Amount of payment by check

WTH

Instructions for Form 306 - Income Tax Withholding Return

Page 2

Who Must File

The Form 306, North Dakota Income

Tax Withholding return must be filed by every employer, even if compensation was not paid during the period covered by this return.

When To File

Except as provided below under “Annual filing,” the Form 306 must be filed for each calendar quarter on or before the following due dates:

Quarter Covered |

Due on or before |

Jan., Feb., March |

April 30 |

April, May, June |

July 31 |

July, Aug., Sept. |

October 31 |

Oct., Nov., Dec. |

January 31 |

Annual filing. Annual filers must file Form 306 for the entire year on or before January 31 following the end of the calendar year.

Part I - Owner Information

Final Returns

If you are out of business, complete Part I of the return. This will enable the Office of State Tax Commissioner to close your account. The

Form 307 and

Part II - Return

Information

Complete lines 1 through 4 to report amount of tax withheld.

Amended Returns

If you incorrectly reported North Dakota income tax withheld in a prior period, you will need to file

an amended return to correct the information.

1.Obtain a blank Form 306 from our website.

2.Fill in the circle (A) indicating this is an amended return.

3.Enter your business name,

address, account number, and the period being amended.

4.Complete Part II - Return Information

a.Enter the correct amount of tax withheld for the period on line 1.

b.Enter the amount of tax paid with the original return (if any) on line 1a.

c.Subtract line 1a from line 1

and enter on line 2. This is the amount of the refund or tax due.

d.Complete lines 3 and 4 to

calculate the total due including any penalty and/or interest.

Penalty And Interest

Provisions

Returns must be filed and the full amount of tax must be paid by the due date of the return. If a return is not filed or if full payment is not made on or before the due date, the law provides for penalty and interest

charges as outlined in our income tax withholding guideline. North Dakota Century Code (N.D.C.C.)

§

Disclosure Authorization

By filling in the circle, you authorize the North Dakota Office of State Tax Commissioner (Tax Department) to discuss matters pertaining to this Form 306 with the contact person

listed.

Part III - Payment

Information

Electronic payments may be made at www.nd.gov/tax/payment. If you are paying by check, complete Part III of Form 306 and make your check payable to North Dakota Tax Commissioner.

For Assistance

Email withhold@nd.gov or call 701.328.1248 or fax 701.328.0146.

Electronic Filing and Payment

Options are available to file and pay electronically through Taxpayer Access Point (TAP). Please go to www.nd.gov/tax/tap for more information.

File Attributes

| Fact Number | Fact Detail |

|---|---|

| 1 | The ND 306 form is titled "Income Tax Withholding Return" and falls under the jurisdiction of the North Dakota Office of State Tax Commissioner. |

| 2 | This form needs to be filled out by employers on a quarterly basis or annually, depending on the filing status they qualify for. |

| 3 | Amendments to previously filed returns are accommodated by marking the specific circle on the form and providing corrected tax withholding information. |

| 4 | Businesses that have changed ownership or that are closing must complete a specific part of the form to notify the North Dakota Office of State Tax Commissioner. |

| 5 | For those who need to correct previously reported tax withheld, specific lines (1 through 4 in Part II) must be completed to adjust the amount. |

| 6 | Late or incorrect filings are subject to penalty and interest charges as per North Dakota Century Code (N.D.C.C.) §57-38-45(2b). |

| 7 | The form enables authorization for the North Dakota Tax Department to discuss the return details with a designated contact person. |

How to Write Nd 306

Filing the Nd 306 form is an essential process for employers in North Dakota to report and pay income tax withheld from their employees' wages. This document ensures compliance with state tax regulations, aiding in the proper management of payroll taxes. The process involves accurately providing business and tax details, calculation of the tax withheld, and submission of this information to the North Dakota Office of State Tax Commissioner. It's crucial for the form to be filled out correctly to avoid any potential penalties or discrepancies. Here is a step-by-step guide to help you through the instructions on filling out the form.

- Visit the official website to download a blank Form 306 or obtain a copy from the North Dakota Office of State Tax Commissioner.

- Identify the type of return you are filing. If amending a previously filed return, fill in the circle labeled (A) to indicate this is an amended return.

- If you have been assigned a new federal ID number, fill in the circle (C) and enter your new ID number in the space provided.

- Mark the circle if your address has changed to update the Tax Commissioner's records with your current address.

- In Part I - Ownership Information, only fill this section if it's a FINAL return. Indicate if you are no longer in business or no longer have employees by filling in the circle (O) and entering the last day of business or employment. If there's a change in ownership, fill in the circle (C) and provide the new owner's details including the name, address, and phone number.

- Proceed to Part II - Return Information:

- Enter the total North Dakota income tax withheld for the period covered by this return on line 1.

- If filing an amended return, enter the North Dakota Tax originally reported on line 1a.

- Calculate the Total Tax Due or Refund by subtracting line 1a (if applicable) from line 1 and enter the result on line 2.

- Enter any penalty or interest amounts if applicable in the spaces provided and add these to the Total Tax Due on line 4.

- Authorize the North Dakota Office of State Tax Commissioner to discuss this return with the contact person listed by filling in the respective circle and providing the contact's details including name and phone number.

- Sign and date the form. The taxpayer needs to sign and include their title and the date the form is being filed.

- In Part III - Payment Information, if paying by check, complete the Taxpayer's Name, Address (including City, State, ZIP Code), Account Number, and the Period Ending. Write the amount of payment by check and attach the payment to the form.

- Mail the completed form along with any payment due to the North Dakota Office of State Tax Commissioner at the provided address on the form.

After submitting this form, it's advisable to keep a copy for your records. Timely and accurate filing of Form 306 helps ensure compliance with North Dakota tax laws and aids in the efficient administration of payroll taxes for your business.

Your Questions, Answered

- What is the Form 306?

Form 306 is an Income Tax Withholding Return used by the North Dakota Office of State Tax Commissioner. It must be filed by every employer in North Dakota who has paid compensation to employees, to report the income tax withheld from their earnings.

- Who needs to file the Form 306?

All employers in North Dakota are required to file the Form 306, even if they did not pay compensation during the period covered by the return.

- When is the Form 306 due?

- For quarterly filers, the due dates are April 30th for Q1, July 31st for Q2, October 31st for Q3, and January 31st for Q4.

- Annual filers must submit their Form 306 by January 31st of the following year.

- How do I file an amended Form 306?

- Download a blank Form 306 from the North Dakota State Tax Commissioner's website.

- Indicate that it's an amended return by filling in the appropriate circle.

- Fill out your business details and the period you're amending.

- Correct the amount of tax withheld and follow steps to calculate any differences, penalties, or interest.

- What happens if I don't file on time?

If the Form 306 is not filed or if the tax due is not paid by the deadline, employers are subject to penalties and interest as defined by the North Dakota Century Code (N.D.C.C.) §57-38-45(2b).

- Can I authorize someone to discuss my Form 306 with the North Dakota Office of State Tax Commissioner?

Yes, by filling in the designated circle on the form, you authorize the Tax Department to discuss details of this return with the contact person you list.

- What should I do if my business address or ownership has changed?

If your business address or ownership changes, you should indicate this on the Form 306 by filling in the appropriate circle and providing the new information as requested on the form.

- How can I make payments for the tax due on Form 306?

Payments can be made electronically via the North Dakota State Tax Commissioner's website or by mailing a check along with Part III of Form 306 to the stated address. Ensure checks are payable to the North Dakota Tax Commissioner.

- What if I am out of business or no longer have employees?

If you're closing your business or if you no longer have employees, complete Part I of Form 306 to inform the Office of State Tax Commissioner, so they can close your withholding tax account accordingly.

- Where can I find more information or get assistance with Form 306?

For additional assistance, you can contact the North Dakota Office of State Tax Commissioner via email at withhold@nd.gov, by phone at 701.328.1248, or via fax at 701.328.0146. Information and electronic filing options are also available on their website.

Common mistakes

Filling out North Dakota's Form 306, the Income Tax Withholding Return, might seem straightforward, but mistakes can easily occur. Understanding these common errors can help ensure the process is done correctly.

- Not updating business information: One of the frequent mistakes is not updating the business information when there has been a change. If your address has changed or if you've been assigned a new federal ID number, it’s crucial to indicate these changes on the form to avoid any processing delays.

- Incorrectly reporting the tax amount: A common error involves inaccurately reporting the total North Dakota income tax withheld for the period. Double-checking your figures against your records can prevent this mistake.

- Failing to file an amended return correctly: If you realize that the information submitted on a previous return was incorrect, you must file an amended return. Ensure you fill in the circle indicating it's an amended return and accurately complete Part II with the corrected information.

- Omitting final return information: If your business is closing or you will no longer have employees, it’s essential to complete Part I to inform the North Dakota Office of State Tax Commissioner properly. Failing to do this can lead to unnecessary follow-ups.

- Not authorizing discussion: If you want the North Dakota Office of State Tax Commissioner to discuss your return with a designated contact person, you must fill in the authorization circle. Skipping this step may hinder effective communication regarding your return.

- Making payment errors: When making a payment, ensure the check is correctly made out to the North Dakota Tax Commissioner and that the payment amount matches what is reported on the form. Discrepancies can delay processing.

- Overlooking electronic filing options: Many businesses are not aware they can file and pay electronically through North Dakota's Taxpayer Access Point (TAP). This mistake can lead to unnecessary paperwork and delay.

- Ignoring due dates: Finally, missing the filing due date can result in penalties and interest charges. Being aware of the filing deadlines for each quarter or the annual filing requirement is crucial.

By avoiding these mistakes, you can help ensure that your Form 305 submission is accurate and compliant, avoiding potential penalties and ensuring smooth operations for your business. Always refer to the latest guidelines provided by the North Dakota Office of State Tax Commissioner to stay informed of any updates or changes to the filing process.

Documents used along the form

When filing the ND 306 form - Income Tax Withholding Return, individuals or businesses often need to complete additional forms and documents to comply with North Dakota tax regulations fully or to address specific situations. These documents can provide further details about your tax status, outline changes in your business, or help rectify previously submitted information. Here are six forms and documents commonly used alongside the ND 306 form:

- Form 307: This form is necessary for employers to report wages paid and taxes withheld for their employees. It's particularly relevant during the final year of operation for a business closing its accounts with the North Dakota Office of State Tax Commissioner.

- W-2 Forms: These are wage and tax statements that employers must provide to each of their employees and to the IRS. These forms detail the employee's income and taxes withheld over the year and are crucial for finalizing individual income tax returns.

- Amendment Forms for previously filed ND 306 returns: If there were errors in a previously filed ND 306 form, amendment forms are used to correct the tax withheld and tax due information. This ensures accuracy in reporting and compliance with state tax laws.

- Electronic Payment Submission: While not a form, making payments electronically is often recommended alongside submitting the ND 306. This process involves using the North Dakota Taxpayer Access Point (TAP) for secure and efficient tax payments.

- Application for Extension of Time to File: This application is used if an employer needs additional time to file their ND 306 form. It helps to avoid penalties by notifying the tax department of a delay in filing.

- Form W-3: The Transmittal of Wage and Tax Statements form summarizes the information contained in the W-2 forms for the IRS. Although primarily federal, it's essential for employers as it accompanies the W-2 forms.

Each of these documents plays a vital role in the accurate and efficient processing of tax-related information between North Dakota employers and the state tax authority. By understanding and utilizing these forms, businesses can ensure compliance, correct errors, update or change business information, and fulfill their tax obligations more effectively.

Similar forms

The ND 306 Form, an Income Tax Withholding Return for North Dakota, shares similarities with several other tax documents due to its function and structure. This form is utilized by employers to report and remit income taxes withheld from employees' wages, a common practice across various tax forms designed for similar purposes.

Form W-2 (Wage and Tax Statement) is one notable document similar to the ND 306 Form. Both are integral to the process of reporting income taxes withheld from employees' wages. The key similarity lies in the necessity to accurately reflect the total income taxes withheld during a specific period. However, while the ND 306 Form focuses on the employer's obligation to report and remit taxes to the North Dakota Office of State Tax Commissioner, Form W-2 provides a detailed account of an employee's annual earnings and the taxes withheld from those earnings to both the employee and the IRS.

Form 941 (Employer's Quarterly Federal Tax Return) is another document that bears resemblance to the ND 306 Form. Both forms are used by employers to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks. The primary similarity is their quarterly filing requirement, aiming to reconcile the taxes withheld from employees' wages with the actual amounts owed to the tax authority. While the ND 306 Form is specific to North Dakota state income tax, Form 941 addresses federal taxes, showcasing the broader scope of tax reporting and remittance.

Form W-4 (Employee's Withholding Certificate), though not a tax return, is related to the ND 306 Form in its role in the withholding tax process. The Form W-4 is filled out by employees to inform employers of their withholding allowances, which in turn influences the amount of federal income tax withheld from their paychecks. The connection to the ND 306 Form comes from the reliance on accurate W-4 information to determine the proper amount of state income tax to withhold. Thus, while the ND 306 Form is used by the employer to report and remit withheld taxes, the W-4 facilitates the initial determination of the withholding amount.

Dos and Don'ts

When completing the Form 306 - Income Tax Withholding Return for the North Dakota Office of State Tax Commissioner, understanding the do's and don'ts can streamline the process and ensure accuracy. Below are key points to keep in mind:

- Do: Fill in the circle if this is an amended return, indicating that corrections are being made to a previously filed return.

- Do: Provide your new federal ID# if you have been assigned one, ensuring all correspondence and records are properly updated.

- Do: Mark the change of address circle if your address has changed from the one previously recorded, to ensure all communications reach you.

- Do: Complete Part I concerning Ownership Information only if you are filing a final return, which is essential for closing your account with accuracy.

- Don’t: Leave the total North Dakota income tax withheld, tax due, or refund calculations blank in Part II. Accurate figures are crucial for a correct assessment.

- Don’t: Forget to calculate and include any penalties or interest if your return is late, as outlined under the North Dakota Century Code (N.D.C.C.) §57-38-45(2b).

- Don’t: Overlook the authorization section that allows the North Dakota Office of State Tax Commissioner to discuss this return with your designated contact person, if clarification or further discussion is needed.

- Don’t: Neglect to sign the return. An unsigned return can be considered incomplete and may delay processing or lead to penalties.

Ensuring all parts of the Form 306 are completed accurately and thoroughly can help avoid delays, penalties, and potential legal complications. Attention to detail, from updating ownership information to correctly authorizing discussions, forms the foundation of a properly submitted tax withholding return.

Misconceptions

There are several common misconceptions about the ND 306 form, also known as the Income Tax Withholding Return for North Dakota. Understanding these misconceptions can help filers navigate the process more effectively and ensure compliance with state tax regulations.

Misconception 1: The ND 306 form is only for businesses with employees.

In reality, every employer must file the Form 306, regardless of whether compensation was paid during the period covered by the return.Misconception 2: You don't need to file the ND 306 form if your business hasn't changed.

Even if your business details or status haven't changed, you still need to file the Form 306 according to the required filing dates. Changes in business details are just additional information to report if applicable.Misconception 3: Amended returns are complicated and different forms are required.

To amend a return, you simply obtain a blank Form 306, fill in the circle indicating it's an amended return, and provide updated information in Part II. It requires the same form with updated information.Misconception 4: The ND 306 form can only be filed by mail.

While mailing is an option, electronic filing and payment options are available and encouraged through the North Dakota Tax Commissioner's website and the Taxpayer Access Point (TAP).Misconception 5: You must be out of business to complete Part I of the form.

Part I is to be completed if it's a final return due to your business being out of business or having no more employees, not just when the business closes permanently.Misconception 6: Penalties are only for late filings.

Penalties and interest can apply for not only late filings but also for late payments or not paying the full amount due by the return due date.Misconception 7: You need to wait for a paper check for your refund.

While not explicitly stated, like electronic filings and payments, refunds can potentially be processed quicker through electronic means, though specific processes should be confirmed with the State Tax Commissioner's office.Misconception 8: The ND 306 form is the only document you need to submit when closing a business.

In addition to Form 306, you'll need to submit Form 307 and W-2s for the year your withholding account is closed, ensuring all tax responsibilities are met.Misconception 9: Personal income taxes can be filed with the ND 306.

The Form 306 is specifically for employers to report income tax withheld. Individuals report their personal income taxes using different forms, depending on their circumstances.

Understanding these key points can help smooth the process of filing and ensure that everything related to income tax withholding is properly handled in compliance with North Dakota's tax laws.

Key takeaways

Understanding how to properly complete and use the Form 306 - Income Tax Withholding Return in North Dakota is essential for employers to ensure compliance with state tax laws. Here are key takeaways from the document:

- All employers in North Dakota must file the Form 306, regardless of whether compensation was paid during the period covered.

- Forms must be filed quarterly, with specific deadlines for each quarter. January through March must be filed by April 30th, April through June by July 31st, July through September by October 31st, and October through December by January 31st. Annual filers have a deadline of January 31st for the previous calendar year.

- If you are no longer in business or no longer have employees, complete Part I to notify the Office of State Tax Commissioner and close your account. However, you must still submit Form 307 and any required W-2s for the year your account is closed.

- If you need to amend a previous return due to incorrect reporting of North Dakota income tax withheld, you must file an amended return. This process involves indicating the amendment, entering correct withholding amounts, and calculating any additional tax due or refund.

- Penalties and interest may be applied for failure to file or pay the full amount of tax by the due date. The North Dakota Century Code outlines these provisions.

- By indicating consent on the form, the North Dakota Office of State Tax Commissioner is authorized to discuss the return with the listed contact person. This is important for clarifying and resolving any issues.

- Electronic payment options are available, as well as the ability to file electronically through the Taxpayer Access Point (TAP). Employers are encouraged to use these resources for convenience and efficiency.

For assistance with Form 306 or any related inquiries, employers can reach out via email, phone, or fax to the provided contact details of the North Dakota Office of State Tax Commissioner.

Browse Popular Documents

North Dakota Filing Requirements - The T-12 form's structured conveys complex tax information in an organized, user-friendly manner.

Sfn Conference 2023 - The form accommodates both individual and organizational filers, making it applicable across a range of scenarios involving care for animals.