Printable Nd St Template

Understanding the complexities of tax reporting and compliance is crucial for businesses operating within North Dakota, and the Form ST—Sales, Use, and Gross Receipts Tax Return plays a pivotal role in this process. Issued by the North Dakota Office of State Tax Commissioner, this form ensures that businesses report their taxable and nontaxable sales, use tax on goods consumed, and the gross receipts tax accurately. It provides for various scenarios such as amendments to previous returns, changes in business ownership or address, and cessation of business operations. With detailed instructions on how to correctly fill in tax amounts, calculate penalties and interests for late submissions, and the procedure for claiming compensation discounts for registered permit holders, the form streamlines the tax filing and payment process. Additionally, it covers the reporting requirements for local option sales, use, and gross receipts taxes for jurisdictions that businesses may have operations in or sales to, including specific instructions for those reporting more than ten local taxes. Tax compliance is supported further by clear do’s and don’ts, ensuring that businesses submit their forms correctly to avoid common mistakes, thereby facilitating smoother interactions with the state’s tax administration.

Form Preview

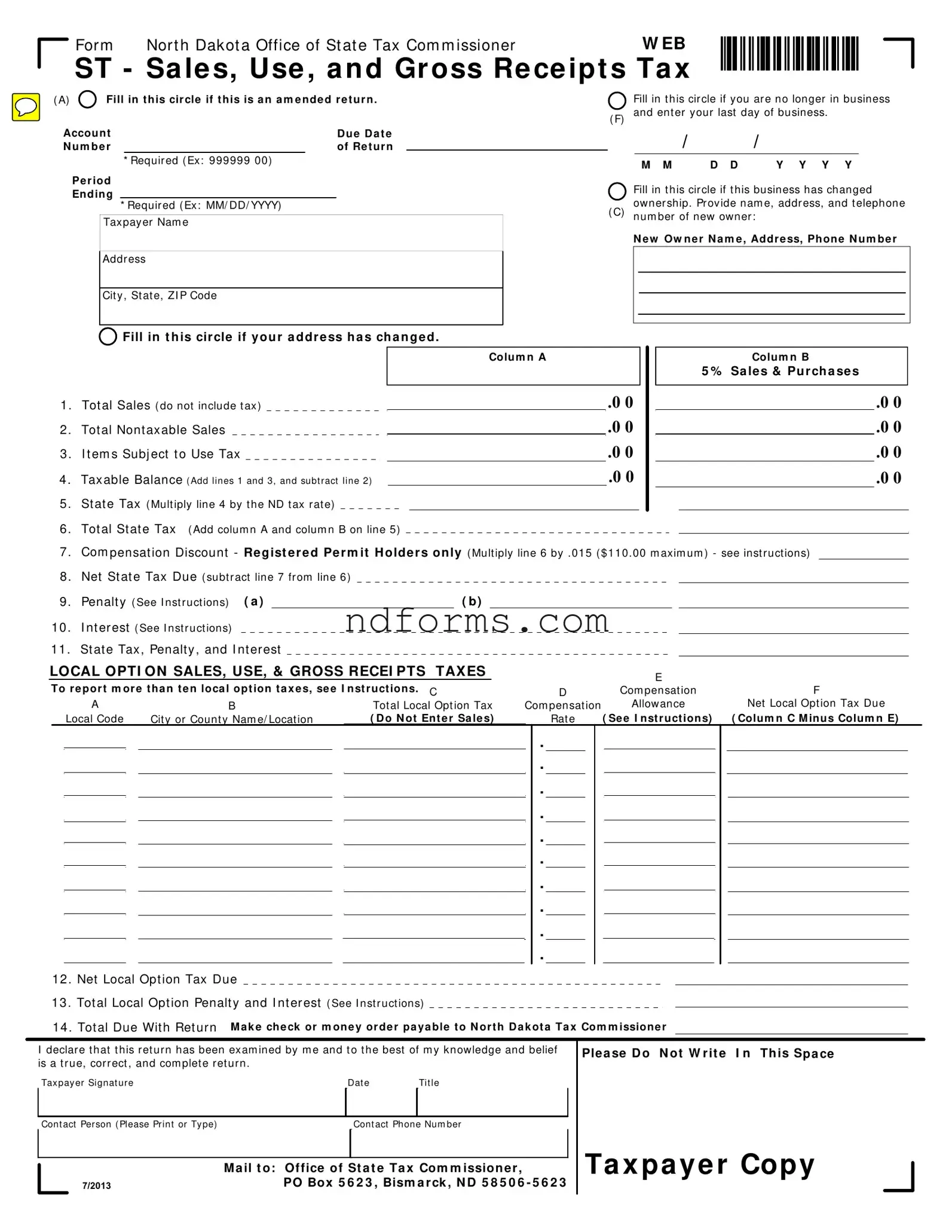

Form Nort h Dakot a Office of St at e Tax Com m issionerW EB

ST - Sa le s, Use , a nd Gr oss Re ce ipt s Ta x

(A)  Fill in this cir cle if this is a n a m e nde d r e tur n.

Fill in this cir cle if this is a n a m e nde d r e tur n.

Account |

|

Due Da t e |

N um be r |

|

of Re t ur n |

* Requir ed ( Ex: 999999 00)

Pe r iod

Ending

* Required ( Ex: MM/ DD/ YYYY) |

( F)

Fill in t his cir cle if you are no longer in business and ent er your last day of business.

/ |

|

/ |

M M |

D D |

Y Y Y Y |

Fill in t his cir cle if t his business has changed owner ship. Pr ovide nam e, addr ess, and t elephone

Taxpayer Nam e |

Address

( C) num ber of new owner :

N ew Ow ner N am e, Address, Phone N um ber

Cit y, St at e, ZI P Code

Fill in t h is circle if you r a ddress h a s ch a n ged .

Fill in t h is circle if you r a ddress h a s ch a n ged .

|

|

|

|

|

Colum n A |

|

|

|

|

|

Colum n B |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

5 % |

Sa les & Pu rch a ses |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 . |

Tot al Sales ( do not include t ax) |

|

|

|

.0 0 |

|

|

|

|

|

|

|

.0 0 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

2 . |

Tot al Nont axable Sales |

|

|

|

.0 0 |

|

|

|

|

|

|

|

.0 0 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

3 . |

I t em s Subj ect t o Use Tax |

|

|

|

.0 0 |

|

|

|

|

|

|

|

.0 0 |

|||||

4 . |

Taxable Balance ( Add lines 1 and 3, and subt ract line 2) |

|

.0 0 |

|

|

|

|

|

.0 0 |

|||||||||

5 . |

St at e Tax ( Mult iply line 4 by t he ND t ax rat e) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

6 . |

Tot al St at e Tax ( Add colum n A and colum n B on line 5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

7 . |

Com pensat ion Discount - Regist ered Perm it H olders only ( Mult iply line 6 by . 015 ( $ 110. 00 m axim um ) - see inst ruct ions) |

|||||||||||||||||

8 . Net St at e Tax Due ( subt r act line 7 from line 6) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

9 . |

Penalt y ( See I nst ruct ions) ( a ) |

|

( b) |

|

|

|

|

|

|

|

||||||||

10 . |

I nt er est ( See I nst r uct ions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

11 . |

St at e Tax, Penalty , and I nt erest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

LOCAL OPTI ON SALES, USE, & GROSS RECEI PTS TAXES |

|

|

|

|

|

|

|

|

|

E |

|

|

|

|

|

|

||||||||||||||||

|

|

To re por t m or e t ha n te n loca l opt ion ta x e s, se e I nst ruct ions. C |

|

|

|

|

|

|

|

|

F |

|||||||||||||||||||||||

|

|

|

|

|

D |

|

|

|

Com pensat ion |

|||||||||||||||||||||||||

|

|

|

|

|

A |

|

B |

|

|

|

|

|

Tot al Local Opt ion Tax |

Com pensat ion |

Allowance |

Net Local Opt ion Tax Due |

||||||||||||||||||

|

|

|

|

Local Code |

Cit y or Count y Nam e/ Locat ion |

( Do N ot Ent e r Sa le s) |

|

|

|

Rat e |

|

|

|

( Se e I nstr uctions) |

( Colum n C M inus Colum n E) |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12 . Net Local Opt ion Tax Due |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

13 . Tot al Local Opt ion Penalt y and I nt erest ( See I nst r uct ions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

14 . Tot al Due Wit h Ret urn |

M a k e che ck or m one y or de r pa ya ble to N or th Da k ot a Ta x Com m issione r |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I declare t hat t his ret urn has been exam ined by m e and t o t he best of m y knowledge and belief |

Plea se D o N ot W rit e |

I n Th is Spa ce |

|||||||||||||||||||||||||||||||

|

is a t r ue, corr ect , and com plet e ret urn . |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

Tax pay er Signat ure |

|

|

|

|

|

Dat e |

|

Tit le |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Cont act Person ( Please Print or Ty pe) |

|

|

|

|

|

Cont act Phone Num ber |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ta x pa ye r Copy |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

M a il t o: |

Office of St a t e Ta x Com m ission er, |

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

7/2013 |

|

|

|

PO Box 5 6 2 3 , Bism a rck , N D 5 8 5 0 6 - 5 6 2 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

For m ST - Sa le s, Use , a nd Gr oss Re ce ipt s Ta x Re t ur n inst r uct ions

General and specifi c line inst ruct ions for Form ST

Ge ne r a l inst r uct ions

Eve r y pe r m it holde r m ust fi le a

r e t ur n for e a ch r e por t ing pe r iod e ve n if no sa le s w e r e m a de or no t a x is due .

A preprinted return, instructions, and return envelope are mailed in the final week of the reporting period to every registered permit holder that fi les a paper return. DO NOT mail a paper return if you

file electronically. For information about electronic filing see www.nd.gov/tax.

Please review the preprinted copy of your return before completing it. The original return has been preprinted specifically for your business.

All r e t ur ns a r e due t he la st da y of t he m ont h follow ing t he r e por t ing pe r iod .

To avoid penalty, the return must be postmarked by the US Postal Service on or before the due date and paid in full with a valid check or money order.

For be st r e sult s, com ple t e t he

or igina l cust om ize d for m a nd m a il it in t he r e t ur n e nve lope pr ovide d .

DO NOT send photocopies. Returns generated from a software package are acceptable if the Tax Commissioner has

I f you use a n a ppr ove d soft w a r e pa ck a ge t o pr e pa r e your r e t ur n it is e sse nt ia l t o e nt e r t he follow ing ide nt ifying infor m a t ion pr ope r ly:

• Account number. Enter the account number as shown on your preprinted form.

• Period ending. Enter the last day of the

• Name and Address. Enter the taxpayer name and address.

Line inst r uct ions - St a t e Ta x e s

Line 1 - Enter the total sales for the reporting period. Do not include the sales tax in this amount.

Line 2 - Enter the total nontaxable sales. Nontaxable sales include:

•Sales to federal, state, and local governments.

•Sales to nursing homes, hospitals, intermediate/basic care facilities, emergency medical services providers licensed by North Dakota Dept.

of Health, assisted living facilities licensed by the North Dakota Dept. of

For m ST

D o’s a nd D on’t s

Do

• Complete and return original forms provided by the Tax Commissioner.

• Print in blue or black ink.

• Print neatly within the designated spaces.

• Round all values in lines 1 through 4 to the nearest whole dollar.

• Enter dollars and cents in lines 5 through 14 and for all local tax data.

Don’t

• Don’t enter dollar signs ($), commas (,), or decimal points (.).

• Don’t use dashes or other symbols to indicate you do not have an entry.

• Don’t use pencil or light colored ink.

• Don’t use Column A unless reporting a state tax rate other than 5%.

Human Services, and voluntary health associations.

•Sales of food and food ingredients for humans excluding prepared food, candy, soft drinks, and dietary supplements.

•Sales of feed, seed, and chemicals used for agricultural purposes.

•Sales of used farm machinery and farm machinery repair parts used exclusively for agricultural purposes (applicable for Farm Machinery Gross Receipts Tax only); electricity; water; steam for ag processing; motor and heating fuel.

•Sales of oxygen, prescription drugs, durable medical equipment for home use,

•Sales to Montana residents who complete a Certifi cate of Purchase on purchases of goods in excess of fifty dollars.

•Sales in interstate commerce (delivered outside North Dakota).

•Sales of nontaxable service.

•Sales for resale or processing.

•

Line 3 – Enter the cost of taxable goods and equipment consumed or used by you that was purchased without tax. For example, items removed from inventory and used by you.

Line 4 – Add lines 1 and 3, and subtract line 2. Enter the result on line 4.

Line 5 – Multiply line 4 by the applicable tax rate and enter the result on line 5.

Line 6 – Add column A and B on line 5 and enter a ount on line 6.

Line 7 – All registered permit holders regardless of fi ling frequency, will receive compensation on each properly filed return. The amount of compensation your company will receive is computed by multiplying the total state tax on line 6 times 1½ percent (.015) and enter the result on line 7. Effective with the

July 1, 2013 return, the compensation may not exceed $110.00 per return. Compensation may not be deducted if the return is fi led after the due date or is not paid in full. Penalty and interest will be assessed on tax due resulting from compensation deduction on a late filed or underpaid return. Please contact our offi ce if a return needs to be amended to ensure the proper vendor compensation rate is used.

Line 8 – Subtract total compensation on line 7 from line 6 and enter the result on line 8.

Line 9 – Calculate penalty if fi ling a late return.

•For the fi rst month the return is late, the penalty is 5 percent of the state tax on line 5 or $5, whichever is greater.

•For each additional month or fraction of a month the return is late, add an additional penalty of 5 percent of the state tax on line 5 up to a maximum of 25 percent.

If items (a) and (b) of line 9 are filled with XXXs, calculate penalty on the total state tax (line 6) and enter in line 9, column B. If items (a) and (b) are blank, calculate penalty on the state tax (line 5) separately for each column, enter the penalty amounts in items

(a)and (b), and enter the total penalty in line 9, column B.

Line 10 – If fi ling a late return, enter the amount of interest due. Interest does not apply to the fi rst month a return is late, but applies at a rate of 1 percent each month or fraction of a month the return remains late or unpaid.

Line 11 – Add lines 8, 9, and 10. Enter the result on line 11.

Loca l opt ion sa le s, use , a nd gr oss r e ce ipt s t a x e s

If you reported more than ten local taxes in the past year, use the Schedule

The Schedule

Inst r uct ions for r e por t ing loca l opt ion t a x e s:

• Report all local tax amounts in dollars and cents.

• Report all local taxes in one place. Do not report some local taxes on Form ST and other local taxes on Schedule

• If you use Schedule

• If you report local taxes in the Local Option Tax section on Form ST, and you are reporting a local tax for the fi rst time, enter the local tax code, name of the city or county, and compensation rate from the list at the bottom of these instructions.

Colum n

Enter the total amount of tax due for each city or county. The tax due is equal to the correct amount of local sales or use tax you should have charged on sales made within the local jurisdiction plus any local use tax due on untaxed goods or services subject to use tax because they were stored, used or consumed within the local jurisdiction.

Colum n

Some local jurisdictions provide compensation to permit holders for collecting and remitting local tax. Multiply the tax in column C times the compensation rate in column D. Compensation may not exceed the maximum amount listed below and is not allowed if the return is late or underpaid. Note: If amount in column C is

negative, enter zero in column E.

Colum n

Subtract the compensation in column E from the total local tax in column C and enter the result.

Line 1 2

Add all of the amounts in column F and enter the result. This is the total amount of local tax due with the return.

Line 1 3

If the return is unpaid or fi led after the due date, a local penalty is due. Penalty and interest, including the minimum $5 penalty, applies separately to each jurisdiction with local tax due. On line 13, enter the total amount of all penalty and interest due on local taxes.

Line 1 4

Add lines 11, 12, and 13 to calculate the total amount due with the return.

M a k e your che ck pa ya ble t o N or t h D a k ot a Ta x Com m issione r .

The taxpayer or taxpayer’s agent must sign the return. Please PRINT the name, title and phone number of a contact person who can answer questions about this return.

Offi ce of St a t e Ta x Com m issione r PO Box 5 6 2 3

Bism a r ck , N D 5 8 5 0 6 - 5 6 2 3 Phone : 7 0 1 .3 2 8 .1 2 4 6

w w w .nd .gov/ t a x

Loca l Opt ion Ta x e s: Code / Jur isdict ion N a m e / Com pe nsa t ion Ra t e / Ta x Ra t e

237 |

Alexander0 |

2% |

106 |

Dickinson0 |

1½% |

143 |

Halliday0 |

1% |

236 |

Lignite0 |

2% |

145 |

New Rockford0 |

.......2% |

223 |

Streeter0 |

1% |

220 |

Anamoose0 |

1% |

209 |

Drake0 |

2% |

158 |

Hankinson4 |

2% |

121 |

Linton2 |

2% |

217 |

New Salem0 |

1% |

231 |

Surrey0 |

2% |

203 |

Aneta0 |

1% |

157 |

Drayton0 |

1½% |

202 |

Hannaford0 |

1% |

136 |

Lisbon0 |

2% |

197 |

Northwood0 |

1½% |

132 |

Tioga0 |

2½% |

162 |

Ashley1 |

1% |

204 |

Dunseith0 |

1% |

112 |

Harvey3 |

2% |

193 |

Maddock0 |

2% |

146 |

Oakes3 |

2% |

195 |

Tower City0 |

2% |

156 |

Beach0 |

1% |

148 |

Edgeley2 |

2% |

222 |

Harwood0 |

1% |

108 |

Mandan3 |

1¾% |

189 |

Oxbow0 |

1% |

170 |

Towner2 |

1% |

133 |

Belfield0 |

2% |

176 |

Edinburg0 |

1% |

164 |

Hatton0 |

2% |

218 |

Mapleton0 |

1½% |

208 |

Page0 |

1% |

182 |

Turtle Lake0 |

2% |

138 |

Berthold0 |

1% |

179 |

Elgin0 |

1% |

180 |

Hazelton2 |

2% |

227 |

Max0 |

1% |

130 |

Park River0 |

2% |

211 |

Underwood0 |

2% |

200 |

Beulah2 |

2% |

131 |

Ellendale2 |

1% |

134 |

Hazen3 |

1½% |

150 |

Mayville0 |

2% |

119 |

Pembina0 |

2½% |

113 |

Valley City0 |

2½% |

229 |

Bisbee2 |

2% |

166 |

Enderlin0 |

2% |

142 |

Hettinger0 |

1½% |

140 |

McClusky0 |

1% |

151 |

Portland0 |

2% |

175 |

Velva0 |

2% |

102 |

Bismarck3 |

1% |

206 |

Fairmount0 |

2% |

168 |

Hillsboro0 |

2% |

188 |

McVille0 |

2% |

154 |

Powers Lake3 |

1% |

111 |

Wahpeton6 |

2% |

122 |

Bottineau2 |

2% |

105 |

Fargo0 |

2% |

172 |

Hoople3 |

1% |

178 |

Medora0 |

2½% |

232 |

Ray0 |

2% |

160 |

Walhalla0 |

2% |

126 |

Bowman0 |

1% |

167 |

Finley0 |

2% |

185 |

Hope0 |

2% |

187 |

Michigan0 |

2% |

198 |

Reeder0 |

1% |

502 |

Walsh Co.0 ............¼% |

|

196 |

Buffalo3 |

2% |

221 |

Forman0 |

1½% |

110 |

Jamestown0 |

2% |

169 |

Milnor0 |

1½% |

152 |

Regent0 |

2% |

505 |

Ward County 0 |

½% |

506 |

Burleigh County3... |

½% |

177 |

Fort Ransom0 |

2% |

117 |

Kenmare0 |

2% |

214 |

Minnewaukan0 |

2% |

159 |

Richardton0 |

2% |

183 |

Washburn3 |

2% |

161 |

Cando2 |

2% |

235 |

Fredonia0 |

2% |

135 |

Killdeer0 |

2% |

103 |

Minot0 |

2% |

199 |

Rolette0 |

2% |

171 |

Watford City3 |

1½% |

124 |

Carrington0 |

2% |

210 |

Gackle0 |

1% |

230 |

Kindred0 |

2% |

216 |

Minto3 |

1% |

125 |

Rolla0 |

2% |

129 |

West Fargo0 |

2% |

191 |

Carson0 |

1% |

139 |

Garrison0 |

2% |

165 |

Kulm0 |

2% |

114 |

Mohall0 |

1% |

118 |

Rugby2 |

2% |

226 |

Westhope0 |

1% |

501 |

Cass County0 |

½% |

219 |

Glenburn0 |

2% |

213 |

Lakota0 |

1% |

507 |

Morton County3 |

½% |

190 |

Scranton0 |

1% |

504 |

Williams County0 |

... 1% |

163 |

Casselton0 |

1% |

212 |

Glen Ullin0 |

1% |

149 |

LaMoure0 |

2% |

153 |

Mott0 |

2% |

233 |

South Heart0 |

2% |

109 |

Williston3 |

2% |

127 |

Cavalier0 |

2% |

107 |

Grafton3 |

2½% |

123 |

Langdon3 |

2% |

173 |

Munich2 |

1% |

186 |

St. John3 |

1% |

184 |

Wilton3 |

2% |

238 |

Center |

2% |

101 |

Grand Forks5 |

1¾% |

128 |

Larimore0 |

1% |

144 |

Napoleon2 |

2% |

137 |

Stanley3 |

1½% |

205 |

Wimbledon0 |

1% |

141 |

Cooperstown0 |

1½% |

225 |

Granville0 |

2% |

234 |

Leeds0 |

2% |

201 |

Neche0 |

2% |

147 |

Steele0 |

2% |

155 |

Wishek3 |

1½% |

116 |

Crosby0 |

3% |

192 |

Grenora0 |

1% |

215 |

Leonard0 |

2% |

194 |

New England0 |

2% |

503 |

Steele County0 |

1% |

224 |

Woodworth0 |

1% |

104 |

Devils Lake3 |

2% |

207 |

Gwinner0 |

2% |

181 |

Lidgerwood0 |

2% |

174 |

New Leipzig0 |

1% |

120 |

Strasburg2 |

2% |

228 |

Wyndmere0 |

2% |

0

1

2

3

4

5

6

The Local tax ordinance does not provide for permit holder compensation.

Compensation rate is 3% up to a maximum amount of $33.33 on a monthly return or $100 on a quarterly return. Compensation rate is 3% up to a maximum amount of $50 on a monthly return or $150 on a quarterly return. Compensation rate is 3% up to a maximum amount of $83.33 on a monthly return or $250 on a quarterly return. Compensation rate is 3% with no maximum.

Compensation rate is 5% up to a maximum amount of $166.67 on a monthly return or $500 on a quarterly return. Compensation rate is 3% up to a maximum of $37.50 per month.

Offi ce of St a t e Ta x Com m issione r , PO Box 5 6 2 3 , Bism a r ck , N or t h D a k ot a 5 8 5 0 6 - 5 6 2 3

Phone : 7 0 1 .3 2 8 .1 2 4 6 , w w w .nd .gov/ t a x

2 1 9 9 7

( I nst r uct ions r e vise d 4 / 1 6 )

File Attributes

| Fact | Detail |

|---|---|

| Form Name | North Dakota Office of State Tax Commissioner WEB ST - Sales, Use, and Gross Receipts Tax |

| Amendment Options | Provides option for amended returns |

| Business Changes | Sections for reporting changes in business ownership or address |

| Reporting Requirements | All permit holders must file a return for each reporting period, regardless of sales made or tax due |

| Compensation Discount | Available for registered permit holders only, with specific calculations and maximum limits |

| Penalties and Interest | Details on penalties and interest for late filings or payments |

| Local Option Taxes | Guidance for reporting more than ten local option taxes, along with detailed instructions for calculation |

| Governing Laws | Regulated under North Dakota state tax laws |

How to Write Nd St

Filling out the North Dakota Sales, Use, and Gross Receipt Slow Ta Return requires attention to detail and accuracy to ensure that your business is in compliance with state tax regulations. The form, also known as Form ST, involves reporting totals of sales, nontaxable sales, and taxable sales, along with calculating the tax owed to the state and, if applicable, local jurisdictions. After completing the form, understanding what comes next is crucial. You're expected to sign and date the form, confirming that the information provided is accurate. Then, you will mail the completed document along with any payment due to the North Dakota Office of the State Tax Commissioner. Compliance with these steps helps in avoiding possible penalties and ensures the timely processing of your tax obligations.

- Identify if you need to check any specific circles at the top concerning amended returns, business closure, or ownership change, and fill in the respective details if applicable.

- Enter your Account Number and the Period Ending Date as required. Ensure these match the details provided on any preprinted form you received.

- Under "Taxpayer Name Address," provide the requested details, and fill in new owner's information if there has been a change in ownership.

- In the section with "Column A Column B 5% Sales & Purchases," carefully input the figures as instructed for Total Sales, Total Nontaxable Sales, Items Subject to Use Tax, and the resulting Taxable Balance. Remember to exclude tax from the total sales figure.

- Calculate the State Tax by applying the ND tax rate to the taxable balance and input your figures for Total State Tax, Compensation Discount if applicable, and then the Net State Tax Due.

- For penalties and interest, refer to the instructions provided if your return is late or incorrect, and calculate these amounts accordingly.

- If you are subject to Local Option Sales, Use, & Gross Receipts Taxes, use the preprinted information or the Schedule ST-Local if reporting on more than ten jurisdictions. Fill out each line with the total local option tax, compensation, and net local option tax due as per the instructions.

- Add the net local option tax due, total local option penalty and interest, and the Total Due With Return. Make sure this figure reflects the sum of all taxes, penalties, and interest due to the state.

- Review the declaration statement, sign, and date the form, ensuring your contact information is clear and accurate.

- Make your check or money order payable to the North Dakota Tax Commissioner, attach it to your form, and mail everything to the address listed for the Office of State Tax Commissioner.

By closely following these steps and double-checking your calculations, you can complete Form ST with confidence. Once mailed, keep a copy of the form and any correspondence for your records. Timely and accurate submission of your tax return maintains your business's compliance and prevents potential issues with the North Dakota Office of the State Tax Commissioner.

Your Questions, Answered

What is the Form ST - Sales, Use, and Gross Receipts Tax? Form ST is a document used by businesses in North Dakota to report and pay sales, use, and gross receipts taxes to the State Tax Commissioner's Office. This form is mandatory for permit holders to complete for each reporting period, even if no sales were made or if no tax is due.

When is Form ST due? The form is due the last day of the month following the end of the reporting period. To avoid any penalty, the form must be postmarked by the due date and the payment must be made in full.

Can Form ST be filed electronically? Yes, electronic filing is available and encouraged for efficiency. Detailed information about electronic filing can be found at the North Dakota Tax Department's website.

What should be included in total sales on Form ST? Total sales should include all sales transactions within the reporting period but should not include the sales tax collected from these transactions.

What qualifies as nontaxable sales on the form? Nontaxable sales can include, but are not limited to, sales to governmental entities, sales to certain healthcare facilities, sales of certain food and agricultural products, and sales for resale or processing. These should be deducted from total sales to find the taxable balance.

How is the taxable balance calculated on Form ST? To find the taxable balance, add the total sales and items subject to use tax, then subtract the total nontaxable sales from this sum.

Is compensation available for filing Form ST? Registered permit holders are eligible for a compensation discount when they file their return on time and pay in full. The discount is calculated as 1.5% of the total state tax due, with a maximum of $110.00 per return effective from July 1, 2013.

How are penalties and interest calculated for late filings? If a return is filed late, a penalty of 5% of the state tax due or $5, whichever is greater, is applied for the first month. For each additional month or fraction thereof, an additional 5% penalty is added, up to a maximum of 25%. Interest is charged at a rate of 1% per month or fraction of a month on any unpaid amount.

How should local option sales, use, and gross receipts taxes be reported? If reporting for ten or fewer local jurisdictions, use the Local Option Tax section on Form ST. For more than ten, use the Schedule ST-Local attachment. Local taxes should be reported in dollars and cents, and the specific instructions provided for each local jurisdiction should be followed.

What documentation is required when changing business ownership or closing a business? When a business changes ownership or ceases operations, specific circles must be filled in on Form ST, and information such as the last day of business or details of the new owner must be provided.

Common mistakes

When filing the North Dakota Office of State Tax Commissioner's Form ST for Sales, Use, and Gross Receipts Tax, careful attention to detail is pivotal. A variety of common mistakes can lead to inaccuracies, potential penalties, or delayed processing times. Understanding these mistakes can help filers ensure their returns are accurate and complete.

First and foremost, a common error is not filling out the form with the correct ink color. The instructions specify the use of blue or black ink, yet filers sometimes overlook this detail. This requirement is likely designed to ensure the form's legibility and the accuracy of scanned documents.

Another mistake involves inaccurate reporting of sales. Filers must enter total sales in line 1 without including the sales tax. This is a critical but often misunderstood step that ensures the tax calculation is based on the correct sales amounts. Moreover, total nontaxable sales must be accurately reported in line 2. These sales can include transactions exempt from tax under North Dakota law, such as sales to government entities or certain non-profit organizations.

Concerning line 3, there's a frequent oversight in reporting items subject to use tax. Items that were purchased without tax for consumption or use by the business must be reported here. Confusion about what constitutes taxable goods for use can lead to either underreporting or overreporting in this section.

- Not reading the preprinted instructions and following the customized information.

- Failing to check the appropriate circles at the beginning of the form for amended returns, business closure, ownership changes, or address changes.

- Incorrectly rounding values or improperly including dollar signs, commas, and decimal points, despite the requirement to round all values to the nearest whole dollar for lines 1 through 4 and to enter dollars and cents as instructed for other lines.

- Overlooking the compensation discount available to registered permit holders, which can reduce the net state tax due.

- Forgetting to calculate penalties and interest correctly for late filings, which can significantly increase the amount owed.

Filers also commonly make errors in the local option taxes section:

- Incorrectly reporting local tax rates or jurisdictions, especially when a new local tax rate applies for the first time.

- Neglecting to calculate or wrongly calculating the compensation allowance and net local option tax due.

- Combining state and local taxes incorrectly, which complicates the overall tax liability.

Finally, an often overlooked but critical step is the signature section. The form requires a signature, printed name, title, and contact number. Filing without this information can result in the return being considered incomplete. Personal attention to these details ensures compliance with North Dakota's tax regulations, promotes accurate tax reporting, and facilitates timely processing by the Tax Commissioner's office.

Documents used along the form

When engaging with the North Dakota Office of State Tax Commissioner for sales, use, and gross receipts tax filings, several forms and documents often come into play alongside the primary Form ST. These documents each serve distinct purposes within the broader context of tax compliance and financial management for businesses. Understanding the role of each form and document is essential for ensuring accurate and timely submissions to state tax authorities.

- Form ST-Local: Designed for businesses reporting more than ten local option taxes. It facilitates detailed reporting for each jurisdiction, ensuring all local sales, use, and gross receipts taxes are correctly accounted for.

- Amended Return Form: Used when corrections need to be made to a previously filed ST form. This form allows taxpayers to adjust reported totals and tax calculations to reflect accurate figures.

- Certificate of Purchase: Required for exempt transactions, such as sales to Montana residents on purchases exceeding fifty dollars, affirming eligibility for a sales tax exemption.

- Business Change Notice: Submitted when there's a change in ownership or business address, ensuring the tax authority has current information for sending notices and correspondence.

- Electronic Filing Waiver Request: For businesses unable to file electronically due to hardship or technical limitations, this request form seeks permission for alternative filing methods.

- Vendor Compensation Claim Form: For registered permit holders eligible for compensation on each properly filed return, this document outlines the process to claim the allowed compensation, ensuring businesses receive any applicable discounts.

Together, these documents and forms interact with the primary Form ST to complete the landscape of sales, use, and gross receipt tax reporting and compliance. They facilitate amendments, account for business changes, enable compliance in specialty situations, and ensure businesses can claim eligible benefits. Through this collection of documentation, businesses can navigate the complexities of tax reporting with greater accuracy and efficiency, ultimately safeguarding their compliance status with the North Dakota Office of State Tax Commissioner.

Similar forms

The Nd St form, formally known as the North Dakota Office of State Tax Commissioner WEB ST - Sales, Use, and Gross Receipts Tax Return, shares similarities with numerous other tax-related documents across various states, primarily due to its structured approach to reporting tax obligations related to sales, use, and gross receipts. This form is meticulously designed to facilitate accurate tax reporting by businesses within the state. Notably, its structured sections for reporting sales, deductions, and tax calculations parallel the organization seen in forms from other states, albeit tailored to North Dakota's tax codes and rates.

One document akin to the Nd St form is the California Sales and Use Tax Return. Like the Nd St form, the California equivalent requires detailed reporting of total sales, taxable and nontaxable sales, and deductions. Both forms calculate taxes due based on applicable rates and provide sections for adjustments such as exemptions or discounts offered to registered permit holders. The primary difference lies in the specific tax rates and the nuances of tax-exempt items, which vary from state to state, reflecting each jurisdiction's unique tax policies and economic objectives.

Another document similar to the Nd St form is the New York State Department of Taxation and Finance's ST-100, Sales and Use Tax Return. Both the Nd St and ST-100 forms share the common goal of accurately determining the tax liability associated with the sale and use of goods and services within their respective states. They include sections for reporting gross sales, taxable sales, and the calculation of taxes owed at state and, if applicable, local levels. The forms also consider special tax rates for specific categories of goods, exemptions, and tax relief provisions custom to their state guidelines. However, the ST-100 form encompasses a broader spectrum of taxes, including region-specific levies, illustrating New York's complex local tax system in contrast to the more streamlined structure seen in North Dakota's tax regime.

These documents, while customized to meet the legislative and regulatory needs of their specific state, underscore a commonality in their foundational purpose: to streamline the process of tax collection. This alignment ensures taxpayer compliance, simplifies administrative procedures, and secures state revenue crucial for public services and infrastructure. Despite their parallels, the subtle distinctions between these forms encapsulate the varied fiscal landscapes across the United States, highlighting the balance between uniformity in tax reporting and the diversity of state-specific tax obligations.

Dos and Don'ts

When preparing to fill out the North Dakota Office of State Tax Commissioner Form ST - Sales, Use, and Gross Receipts Tax Return, it's important to pay close attention to both the details and the requirements. Here are key dos and don'ts to keep in mind:

Things you should do:

- Ensure that you complete and return the original forms that were provided to you by the Tax Commissioner to prevent any processing delays.

- Use blue or black ink when filling out the form for clarity and to ensure that all information is legible.

- Stay within the designated spaces when printing information to keep the form neat and readable.

- Round all values to the nearest whole dollar for lines 1 through 4, but remember to enter dollars and cents for lines 5 through 14 and for all local tax data.

Things you shouldn't do:

- Do not enter dollar signs ($), commas (,), or decimal points (.) within the number fields as this can cause confusion and potentially incorrect processing of your form.

- Avoid using dashes or other symbols as placeholders if you do not have an entry for a field; leave it blank instead.

- Do not use pencil or light-colored ink that can fade or be hard to read, as your form needs to be legible when being reviewed by the Tax Commissioner's office.

- Refrain from using Column A unless you are reporting a state tax rate other than the 5%. This ensures that your tax calculations are accurate and in compliance with North Dakota tax laws.

Misconceptions

There are several misconceptions regarding the North Dakota Sales, Use, and Gross Receipts Tax Return, Form ND ST. Addressing these misconceptions can help taxpayers better understand their obligations and the process of completing and submitting the form accurately.

- Misconception 1: Electronic filers need to mail a paper return. The state encourages electronic filing and does not require a paper return from those who file electronically, streamlining the process for both the taxpayer and the state's processing system.

- Misconception 2: All sales are taxable. The form differentiates between taxable and nontaxable sales, including exemptions for certain goods and services, sales for resale, and sales to tax-exempt organizations.

- Misconception 3: The compensation discount is automatically applied to all returns. This compensation is provided to registered permit holders who file their return correctly and on time, but it cannot exceed a specific maximum amount and is not given if the return is filed late or not paid in full.

- Misconception 4: Taxpayers must calculate taxes for each local jurisdiction separately if they exceed ten jurisdictions. Taxpayers can use the Schedule ST-Local to report taxes for multiple jurisdictions, simplifying the reporting process for those with widespread sales.

- Misconception 5: Dollar signs, commas, or decimal points need to be included in the return. The instructions specify not to use these symbols when entering amounts, ensuring consistency and reducing processing errors.

- Misconception 6: The form must be printed in black ink only. While blue or black ink is preferred to ensure legibility, the key requirement is to avoid pencil or light-colored inks that might not be scanned properly.

- Misconception 7: Personal assets consumed or used in the business are not taxable. Taxpayers are required to report the use tax on taxable goods and equipment consumed or used by their business that were purchased without tax.

- Misconception 8: Trade-ins and returned merchandise do not affect taxable sales. The form allows taxpayers to deduct trade-in allowances and returned merchandise from their total taxable sales, thus potentially lowering the amount of sales tax due.

Understanding these nuances ensures compliance and accuracy in fulfilling state tax obligations, and helps taxpayers avoid common pitfalls associated with the preparation and submission of Form ST. It's vital for taxpayers to carefully review the specific line instructions and general guidelines provided with the form to ensure accurate reporting.

Key takeaways

When managing the North Dakota State (ND ST) form for Sales, Use, and Gross Receipts Tax, it is crucial to navigate the document with precision and understanding. Here are key takeaways to consider:

- Ensure to indicate on the form if it's an amended return by filling in the specified circle at the top.

- Clearly state if the business ownership has changed, ceased, or if there's been a change in business address, by filling in the respective circles and providing the necessary details.

- Total sales reported should exclude sales tax to avoid inaccuracies in tax calculation.

- It's important to distinguish between taxable and nontaxable sales, where nontaxable sales might include, but are not limited to, sales to government entities, certain nonprofit organizations, and sales of specific items exempt from tax under North Dakota law.

- For goods used or consumed by the business that were not initially taxed at purchase, report these in the 'Items Subject to Use Tax' section.

- Calculate the taxable balance carefully by adding total sales and taxable use, then subtracting nontaxable sales, to ensure the accuracy of state tax computation.

- Registered permit holders are eligible for a compensation discount on the state tax owed, but it's crucial to file the return timely and pay in full to qualify for this benefit.

- Penalties and interest are assessed for late filings or payments, with specific calculation instructions provided in the form.

- Local option taxes require careful reporting based on jurisdiction codes and compensation rates, which are crucial for accurate local tax assessment.

- Always review the preprinted form and instructions sent by the North Dakota Office of State Tax Commissioner to ensure compliance with the latest guidelines and tax rates.

- Electronic filing is encouraged, and detailed instructions are available on the North Dakota government website to facilitate this process.

By adhering to these guidelines, filers can navigate the complexities of the ND ST form more effectively, ensuring accurate and compliant tax reporting.

Browse Popular Documents

North Dakota Nonresident Filing Requirements - Filers can indicate if the form is for a joint return and specify the filing status used on their federal return.

51/50 Law - A vital component of the mental health legal system in North Dakota, aiming to protect individuals from harm due to untreated mental illness or substance abuse.