Printable North Dakota 307 Template

The North Dakota Form 307 plays an integral part in the process of annual wage and tax statement transmittals for employers within the state. This specific form is utilized to report the total North Dakota state income tax withheld from employees' wages and various payments indicated on W-2 and 1099 forms. It is designed for those subject to North Dakota's income tax withholding obligations, including those who have not withheld any state income tax. The requirement of Form 307 extends beyond active businesses to encompass those that have closed their accounts during the tax year. Additionally, the form outlines a directive for employers to file W-2 and 1099 forms either electronically or on magnetic media if they meet certain criteria, encouraging a move towards digital submission for efficiency and accuracy. Detailed instructions on the completion and submission of Form 307, including specific mailing addresses and deadlines, underline the state's efforts to streamline the process. Moreover, the instructions highlight necessary steps for businesses that have concluded operations, emphasizing the importance of proper closure filings. As a tool for compliance and communication between businesses and the state tax department, Form 307 represents a critical document in the administrational framework of North Dakota's tax obligations.

Form Preview

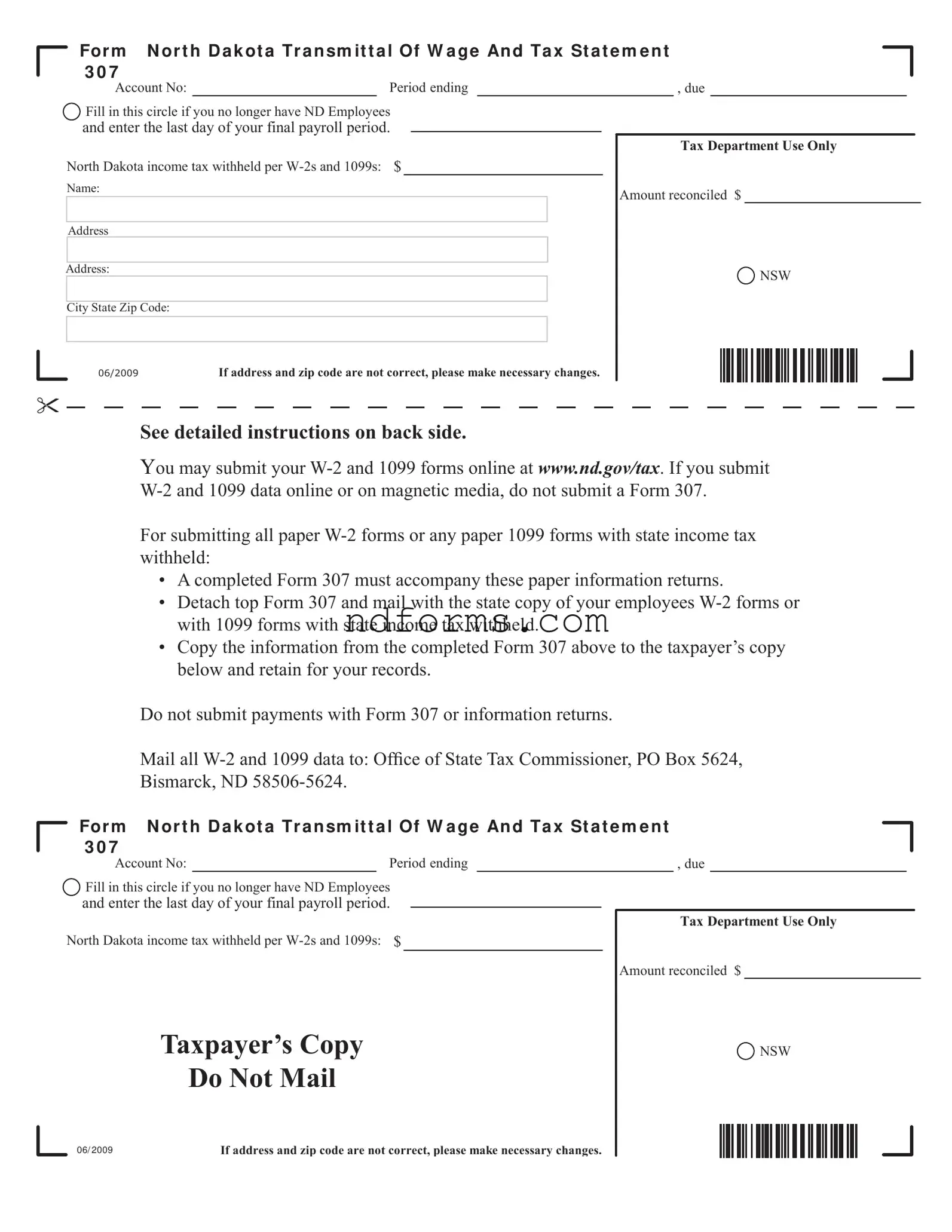

For m N or t h D a k ot a Tr a n sm it t a l Of W a g e An d Ta x St a t e m e n t 3 0 7

Account No: |

|

Period ending |

Fill in this circle if you no longer have ND Employees

Fill in this circle if you no longer have ND Employees

and enter the last day of your final payroll period.

North Dakota income tax withheld per

Name:

Address

Address:

City State Zip Code:

, due

T x Dep rtment UVe Only

Amount reconciled $

NSW

NSW

|

If ddreVV nd zip code re not correct, ple Ve m ke neceVV ry ch nJeV. |

See detailed instructions on back side.

You may submit your

For submitting all paper

•A completed Form 307 must accompany these paper information returns.

•Detach top Form 307 and mail with the state copy of your employees

•Copy the information from the completed Form 307 above to the taxpayer’s copy below and retain for your records.

Do not submit payments with Form 307 or information returns.

Mail all

Bismarck, ND

Fo r m N or t h D a k ot a Tr a n sm it t a l Of W a g e An d Ta x St a t e m e n t 3 0 7

Account No: |

|

Period ending |

Fill in this circle if you no longer have ND Employees

Fill in this circle if you no longer have ND Employees

and enter the last day of your final payroll period.

North Dakota income tax withheld per

Taxpayer’s Copy

Do Not Mail

, due

Tax Department Use Only

Amount reconciled $

NSW

NSW

06/ 2009 |

If address and zip code are not correct, please make necessary changes. |

Instructions

Who Must File Information Returns with Form 307

•An employer subject to North Dakota’s income tax withholding law, whether or not the employer withheld North Dakota income tax. The employer must submit a copy of each

•Any person who voluntarily withheld North Dakota income tax from a payment for which the person is required to fi le a Form 1099 with the Internal Revenue Service. The person must submit a copy of each Form 1099 reporting a payment from which North Dakota income tax was withheld.

•Paper Form 307 must be completed and returned to the Offi ce of State Tax Commissioner even though you may have closed your account during the tax year.

•Corrections to

at

Requirement to File Electronically or on Magnetic Media

You must submit the

How to Complete Form 307

Form 307 is mailed to all employers registered to withhold North Dakota state income tax from wages or other payments and to employers that are not required to register but have previously submitted information returns as required by law. Form 307 is not required to be filed if information returns are submitted electronically or on magnetic media. When submitting all paper

•If you no longer have employees and do not have information returns to submit, fi ll in the circle indicating you do not have employees, enter the date of your last payroll, and mail the Form 307 to the Tax Commissioner.

•If you submit your information returns on paper, you must complete and submit a Form 307 and a copy of all

•If you fi led and submitted North Dakota income tax withholding under more than one identifi cation number during the reporting year, please submit a letter with this information.

•Mail magnetic media to: Offi ce of State Tax Commissioner, 600 E. Boulevard Ave., Dept. 127, Bismarck, ND

•Mail Form 307 with paper information returns to: Offi ce of State Tax Commissioner, PO Box 5624, Bismarck, ND

When to File

If Still in Business:

If Out of Business:

Forms and Assistance

If you have questions or need forms, you may contact the Income Tax Withholding Section at

www.nd.gov/tax or by writing to our offi ce at the above address. |

I N ST R U CT ION S REV ISED 1 0 / 2 0 0 9 |

File Attributes

| Fact Number | Fact Detail |

|---|---|

| 1 | The North Dakota Form 307 is used for the Transmittal of Wage and Tax Statements. |

| 2 | Employers who are subject to North Dakota's income tax withholding laws are required to file Form 307 alongside copies of each W-2 form submitted to the Social Security Administration. |

| 3 | Individuals or entities that voluntarily withhold North Dakota income tax on payments requiring a Form 1099 must also submit Form 307 with each relevant 1099 form. |

| 4 | If an employer or payer has ceased having North Dakota employees during the tax year, they are still required to submit a completed Form 307, indicating the date of their last payroll period. |

| 5 | Corrections to previously submitted W-2 forms should be made with a Federal Form W-2C, which should also accompany a state Form 307 when sent to the Office of State Tax Commissioner. |

| 6 | Employers required to file W-2 and 1099 forms electronically or on magnetic media with the IRS, and have 250 or more forms for North Dakota, must also submit those forms electronically or on magnetic media to North Dakota. |

| 7 | Form 307 is not required if submitting W-2 and 1099 data electronically or on magnetic media, except when paper submissions are made. |

| 8 | The completed Form 307 along with paper W-2s or 1099s with North Dakota income tax withheld should be mailed to the Office of State Tax Commissioner, with a specific PO Box in Bismarck, ND, designated for these submissions. |

| 9 | Submission deadlines for W-2 and 1099 data (including the Form 307 if required) are on or before February 28 of the following year if still in business, or concurrently with final Federal W-3 and W-2 filings if out of business. |

| 10 | Employers and payers can obtain additional forms and assistance for completing Form 307 through the Income Tax Withholding Section by phone, Relay North Dakota for the speech and hearing impaired, or the official North Dakota tax website. |

How to Write North Dakota 307

Filling out the North Dakota 307 Form, titled Transmittal of Wage and Tax Statement, is an essential step for employers who need to submit paper W-2 and 1099 forms with state income tax withheld to the North Dakota Office of State Tax Commissioner. This procedure ensures compliance with state tax laws, facilitating the accurate processing of tax documents. For those submitting these forms, it's crucial to follow the prescribed steps meticulously to avoid errors that could lead to delays or penalties.

- Start by identifying whether you're still in business or if you've closed your North Dakota operations. If you've ceased operations, fill in the circle indicating you no longer have ND employees and enter the date of your last payroll on the specified line at the top of the form.

- Input the total North Dakota income tax withheld from W-2s and 1099s in the designated fields. Ensure the amount is accurate to avoid discrepancies.

- Fill in your employer details accurately, including the Account No., name, and address (street, city, state, and zip code).

- If your address or zip code has changed, make the necessary amendments on the form to ensure your records are updated.

- Attach an adding machine tape that totals the North Dakota withholding amount if you're submitting paper copies of W-2 or 1099 forms. This step is crucial for verifying the total income tax withheld.

- Detach the top portion of Form 307 and mail it along with the state copy of your employees' W-2 forms or any 1099 forms with state income tax withheld to the Office of State Tax Commissioner at PO Box 5624, Bismark, ND 58506-5624.

- Copy the filled-out information from the completed Form 307 to the taxpayer’s copy located at the bottom of the form. Retain this portion for your records, providing a reference and proof of submission.

- Ensure that all paper W-2 and 1099 forms are separated before mailing them with the completed Form 307.

- If information returns were submitted under more than one identification number during the reporting year, include a letter with this form detailing each identification number used.

- Review the form for accuracy, ensuring that all filled sections are correct and all required attachments are included. Submit the form and attachments by mail to the designated address.

Remember, if you are required to file electronically or on magnetic media with the IRS and have 250 or more forms to file with North Dakota, you must adhere to these same guidelines for state submissions. For those who have migrated to electronic filing or use magnetic media, Form 307 is not required. Always verify the current filing requirements and deadlines on the North Dakota Tax Department's website to maintain compliance and ensure timely submissions.

Your Questions, Answered

Who needs to file Form 307?

Form 307 must be filed by any employer subject to North Dakota's income tax withholding law, regardless of whether North Dakota income tax was actually withheld. This includes employers who are required to file W-2 forms with the Social Security Administration and any individual responsible for filing Form 1099 with the IRS from which North Dakota income tax was withheld. Additionally, if you have closed your North Dakota withholding account during the tax year, you must still complete and submit a Form 307.

What if I submit W-2 and 1099 information electronically or on magnetic media?

If you file your W-2 and 1099 forms electronically with the IRS or on magnetic media, and the quantity of forms being filed with North Dakota is 250 or more, you are not required to submit a paper Form 307. Employers are encouraged, but not required, to file electronically if the number of forms submitted to North Dakota is less than 250.

How do I complete Form 307?

To complete Form 307, start by entering the total North Dakota state income tax withheld as shown on your W-2s or 1099 forms on the form's dollar line. Attach an adding machine tape totaling the North Dakota withholding amounts, and submit this along with your paper information returns. Make sure to copy the completed information to the Taxpayer’s Copy section for your records. If you no longer have North Dakota employees, indicate this on the form by filling in the specified circle and include the date of your last payroll.

What is the deadline for filing Form 307?

For entities that are still in business, all W-2 and 1099 data, along with Form 307 if required, must be filed with the Office of State Tax Commissioner by February 28 of the year following the reporting year. If your business is closing, you should file the information at the same time as your final Federal Forms W-3 and W-2 with the IRS.

Where should I send Form 307 and the associated documents?

- For paper information returns, mail Form 307 and the state copies of your employees' W-2 forms or any 1099 forms with state income tax withheld to the Office of State Tax Commissioner, PO Box 5624, Bismarck, ND 58506-5624.

- For forms filed electronically or on magnetic media, no Form 307 is needed.

- When mailing magnetic media, use the address: Office of State Tax Commissioner, 600 E. Boulevard Ave., Dept. 127, Bismarck, ND 58505-0599.

Where can I get help or additional forms?

If you have questions or need additional forms, you can contact the Income Tax Withholding Section at (701) 328-1248. Speech and hearing impaired individuals may call through Relay North Dakota at 1-800-366-6888. Forms and guidelines are also available online at www.nd.gov/tax or by writing to the Office of State Tax Commissioner at the address provided above.

Common mistakes

Filling out the North Dakota 307 form, which is essential for employers reporting wages and tax statements, can be straightforward. However, individuals often make mistakes that can lead to delays or errors in processing. Let's discuss some of the most common pitfalls to avoid.

One key mistake is failing to accurately report the total North Dakota state income tax withheld as shown on Forms W-2 or 1099. This figure should be entered on the form along with an adding machine tape detailing the withholding amount. Accuracy here is crucial for the state to reconcile your tax obligations properly.

Another common error is not properly indicating a business closure. If you no longer have employees and are submitting this form as part of closing operations, you must fill in the designated circle and enter the last day of your final payroll period. This notifies the Office of State Tax Commissioner correctly and ensures they don't expect future submissions.

Many also forget to submit a Form 307 when using paper W-2 or 1099 forms with state income tax withheld. The requirement still stands even if you've previously filed electronically or through magnetic media. Failing to comply can result in unprocessed submissions.

- Incorrectly filling out or omitting the account number and period ending details, which are critical for identifying the reporting business and the relevant tax period.

- Not detaching the top Form 307 to mail with the state copy of your employees' W-2 forms or with the 1099 forms that have state income tax withheld.

- Overlooking the instructions to separate all paper W-2 and 1099 forms before submitting, which helps streamline the processing on the tax department's end.

- Submitting forms with outdated or incorrect business addresses and zip codes, which could delay or misdirect essential correspondence from the tax department.

- Missing the filing deadline, which is on or before February 28 of the following year if still in business, or the time of filing final Federal Forms W-3 and W-2 if going out of business.

- Failure to maintain a copy of the completed Form 307 for records, as indicated by the instructions to copy the information into the Taxpayer’s Copy section before mailing.

To sum up, paying close attention to the form's specifics and avoiding these mistakes can ensure that your North Dakota 307 form is submitted correctly and processed efficiently. Remember, when in doubt, refer back to the included instructions or contact the income tax withholding section for guidance.

Documents used along the form

When submitting the North Dakota Transmittal of Wage and Tax Statement (Form 307), individuals or businesses are often required to include additional forms and documents to ensure compliance with tax regulations. The importance of these supplementary documents cannot be overstated as they collectively provide a comprehensive overview of an entity's financial obligations and payroll details to the North Dakota Office of State Tax Commissioner. Below are five such documents typically used alongside Form 307.

- W-2 Forms (Wage and Tax Statements): These forms are essential for reporting an employee's annual wages and the amount of taxes withheld from their paycheck. Every employer engaged in a trade or business who pays remuneration for services performed by an employee, including non-cash payments, must file a Form W-2 for each employee from whom income, social security, or Medicare tax was withheld.

- 1099 Forms: This set includes various forms used to report income other than wages, salaries, and tips. For instance, Form 1099-MISC is used to report payments made to independent contractors (self-employed individuals). If there was North Dakota income tax withheld from any payment reported on a 1099 form, it must accompany the Form 307 submission.

- W-3 Form (Transmittal of Wage and Tax Statements): This form summarizes the information on all of the W-2 forms an employer has issued. It is sent to the Social Security Administration along with a copy of the W-2 forms. Although it is a federal form, it supports the documentation provided in Form 307 by showing the total payroll wages and taxes withheld.

- W-2C Form (Corrected Wage and Tax Statement): This is used to correct errors on previously filed W-2 forms, such as incorrect employee name, Social Security number, or amounts. If corrections are made that affect the state taxes withheld, a corresponding adjustment might need to be included with the Form 307 submission.

- State Tax Registration Forms: For new employers or businesses, registering with the North Dakota Office of State Tax Commissioner is necessary before submitting Form 307. This registration process involves completing certain forms that designate the entity as an employer and establish its responsibility for withholding and remitting state income taxes.

Together with Form 307, these documents create a full record of employment tax responsibilities and contributions for businesses operating in North Dakota. Proper understanding and management of these documents ensure compliance with North Dakota’s tax laws and support the accurate and timely reporting of income taxes withheld from employees and other payees. It is advisable for businesses to consult with a tax professional or legal advisor to ensure all paperwork is correctly prepared and submitted, notably when dealing with specialized situations or corrections.

Similar forms

The North Dakota 307 form, designated for the transmittal of wage and tax statements, has notable similarities with several other tax forms used across the United States. Primarily, it serves as a conduit for reporting state income tax withholding details from W-2 and 1099 forms. Its similarity to other documents can be attributed to its purpose, structure, and the requirements it fulfills for tax reporting.

Federal Form W-3 (Transmittal of Wage and Tax Statements): Just as the North Dakota 307 form accompanies W-2 or 1099 forms with state income tax withheld, the Federal Form W-3 is used to submit W-2 information to the Social Security Administration. Both forms act as summaries for the accompanying documents, consolidating information for easy processing by the respective tax authorities. The key similarity lies in their role as a transmittal document, intended to summarize and transmit employee wage and tax information from multiple forms into a single submission. However, while Form 307 is specific to North Dakota for state tax purposes, Form W-3 fulfills this role on a national level for federal taxes.

Form 1096 (Annual Summary and Transmittal of U.S. Information Returns): Similar to the North Dakota 307, Form 1096 is used to summarize 1099 forms when submitted on paper to the Internal Revenue Service (IRS). The primary function of both forms is to serve as a cover sheet that reports the total amount of payments or withholding being reported to the tax authority. Though Form 1096 pertains to various types of 1099 forms for the IRS, and the 307 Form specifically addresses North Dakota state tax withholdings, their use as summary transmittal forms underscores their similarity. Each is essential for paper filers who need to report multiple forms of income, deductions, or withholdings to different branches of the tax administration.

State-Specific W-3 Forms: Many states have their version of a W-3 form used to transmit wage and tax statements for state income tax purposes, mirroring the function of the North Dakota 307 form. These state-specific W-3 forms gather withheld state income tax information to be filed with the state's tax department, similar to how the 307 Form operates for North Dakota. Despite each state having unique requirements and form layouts, the overarching purpose aligns with that of North Dakota's 307 form - to consolidate and report employee tax withholdings. This parallel function is crucial for maintaining organized and efficient tax reporting systems at the state level.

Dos and Don'ts

When filling out the North Dakota Transmittal of Wage and Tax Statement 307 form, it's important to follow specific guidelines to ensure the process is done correctly. Here’s a list of things you should and shouldn't do:

What to Do:- Ensure Accuracy: Double-check the account number and the period ending information to ensure they are correct.

- Report Total Withholding: Accurately report the total North Dakota income tax withheld as shown on Forms W-2 or 1099 in the designated dollar line.

- Attach Adding Machine Tape: If submitting paper forms, attach an adding machine tape totaling the North Dakota withholding amount.

- Retain a Copy: Copy the information from the completed Form 307 to the Taxpayer’s Copy section and keep it for your records.

- Separate Forms: If submitting paper forms, separate all W-2 and 1099 forms before mailing.

- Use the Correct Mailing Address: Mail Form 307 with paper information returns to the Office of State Tax Commissioner, PO Box 5624, Bismarck, ND 58506-5624.

- File on Time: Submit W-2 and 1099 data (and Form 307 if required) by February 28 of the following year if still in business.

- Don’t Submit Electronically if Unnecessary: Do not submit Form 307 if you’ve submitted your W-2 and 1099 data online or on magnetic media.

- Avoid Inaccuracies: Do not fill in inaccurate information regarding the total North Dakota income tax withheld.

- Don’t Forget to Sign: Fail to sign and date the form where required.

- Don’t Use Outdated Forms: Avoid using outdated versions of Form 307 or any other forms.

- Don’t Miss Including Required Attachments: Neglect to attach any required documents, such as the adding machine tape if submitting paper forms.

- Don’t Mail to the Wrong Address: Avoid mailing forms to an incorrect address.

- Don’t Mix Forms: Do not mix W-2s and 1099s in the same packet without separating them.

Misconceptions

When dealing with tax and wage statements, it's crucial to navigate the process accurately, especially when it involves specific forms like the North Dakota 307 Form. Despite clear instructions, misconceptions about this form often arise, leading to confusion and potentially incorrect filings. Here, we'll clarify four of these common misunderstandings.

- Misconception 1: The ND 307 Form is required for all businesses.

Not all businesses need to submit the ND 307 Form. Only those employers subject to North Dakota's income tax withholding law, or those who voluntarily withheld North Dakota income tax from a payment requiring a Form 1099 with the IRS, must submit this form. Additionally, if an employer has already submitted their W-2 and 1099 data electronically or on magnetic media, filing the Form 307 is unnecessary. This detail helps streamline the process for those who have moved towards digital submissions.

- Misconception 2: Form 307 must be filed even if you no longer have ND employees.

This misunderstanding might lead to unnecessary paperwork. If a business no longer has North Dakota employees and thus, no wage and tax statement to report, they simply fill in the indicated circle on the form, stating they don't have employees, and provide the last payroll date. Sending the form in this scenario actually helps the Tax Commissioner's office maintain accurate records and saves time for both parties.

- Misconception 3: Corrections to W-2 forms cannot be made through the ND 307 Form.

Corrections related to W-2 forms should indeed be made but through the Federal Form W-2C, not directly on the ND 307 Form. This approach ensures that corrections are standardized and recognized at both the federal and state levels, promoting consistency in tax records and minimizing confusion for employers, employees, and tax agencies alike.

- Misconception 4: Paper filings are the only method for the ND 307 Form.

Many assume that the North Dakota 307 Form can only be submitted in paper format. However, the instruction clearly encourages filing the associated W-2 and 1099 forms electronically or on magnetic media, especially if the volume exceeds 250 forms. This digital submission not only expedites processing but also reduces the risk of errors, offering a more efficient way to fulfill state tax obligations.

Clearing up these misconceptions ensures that businesses can handle their North Dakota Form 307 filings more confidently and efficiently, staying compliant with state tax requirements while minimizing administrative burdens.

Key takeaways

Filling out and using the North Dakota Transmittal of Wage and Tax Statement (Form 307) correctly is crucial for employers. This guide aims to provide a clear understanding of the process and key points to remember, ensuring compliance with North Dakota state tax regulations.

Who Needs to File: Form 307 must be filed by employers subject to North Dakota's income tax withholding law, regardless of whether or not North Dakota income tax was actually withheld. Additionally, anyone who has voluntarily withheld North Dakota income tax from a payment, and is required to file a Form 1099 with the IRS, needs to submit a Form 307 along with a copy of each relevant W-2 and Form 1099.

Electronic Submission Requirements: If an employer is required to file W-2 and 1099 forms electronically or on magnetic media with the Internal Revenue Service, and the quantity of forms to be filed with North Dakota is 250 or more, then the submission must also be done electronically or on magnetic media. Employers filing fewer than 250 forms are encouraged, though not required, to file electronically to streamline the process.

Paper Submission Details: When submitting paper W-2 or any paper 1099 forms that have state income tax withheld, a completed Form 307 must accompany these submissions. It's important to enter the total North Dakota state income tax withheld as shown on these forms, attach an adding machine tape totaling the North Dakota withholding amount, and ensure all paper forms are separated prior to submission.

Submission Deadlines: For those still in business, the deadline for filing Form 307, alongside W-2 and 1099 data, is February 28th of the following year. If the business is closing, these documents need to be filed concurrently with the final Federal Forms W-3 and W-2 with the IRS.

Filing Corrections and Additional Information: Corrections to previously filed W-2 forms should be made using Federal Form W-2C. If an employer has filed and submitted North Dakota income tax withholding under more than one identification number during the reporting year, a letter detailing this information must be included with the submission. Moreover, if an employer no longer has employees and is not submitting information returns, they should indicate this on Form 307 by filling in the indicated circle and stating the date of the last payroll.

For further assistance or to obtain additional forms, employers are encouraged to contact the North Dakota Income Tax Withholding Section. This form is a vital document for employers in North Dakota, ensuring that tax obligations related to employee wages are accurately reported and processed. By paying close attention to the requirements and deadlines outlined above, employers can avoid common mistakes and ensure their compliance with state tax laws.

Browse Popular Documents

51/50 Law - A provision within the legal system for addressing cases where individuals may not recognize their need for treatment, allowing intervention through court orders.

North Dakota Filing Requirements - Complex calculations are simplified with structured input fields for gross production and extraction taxes.