Printable North Dakota 38 Template

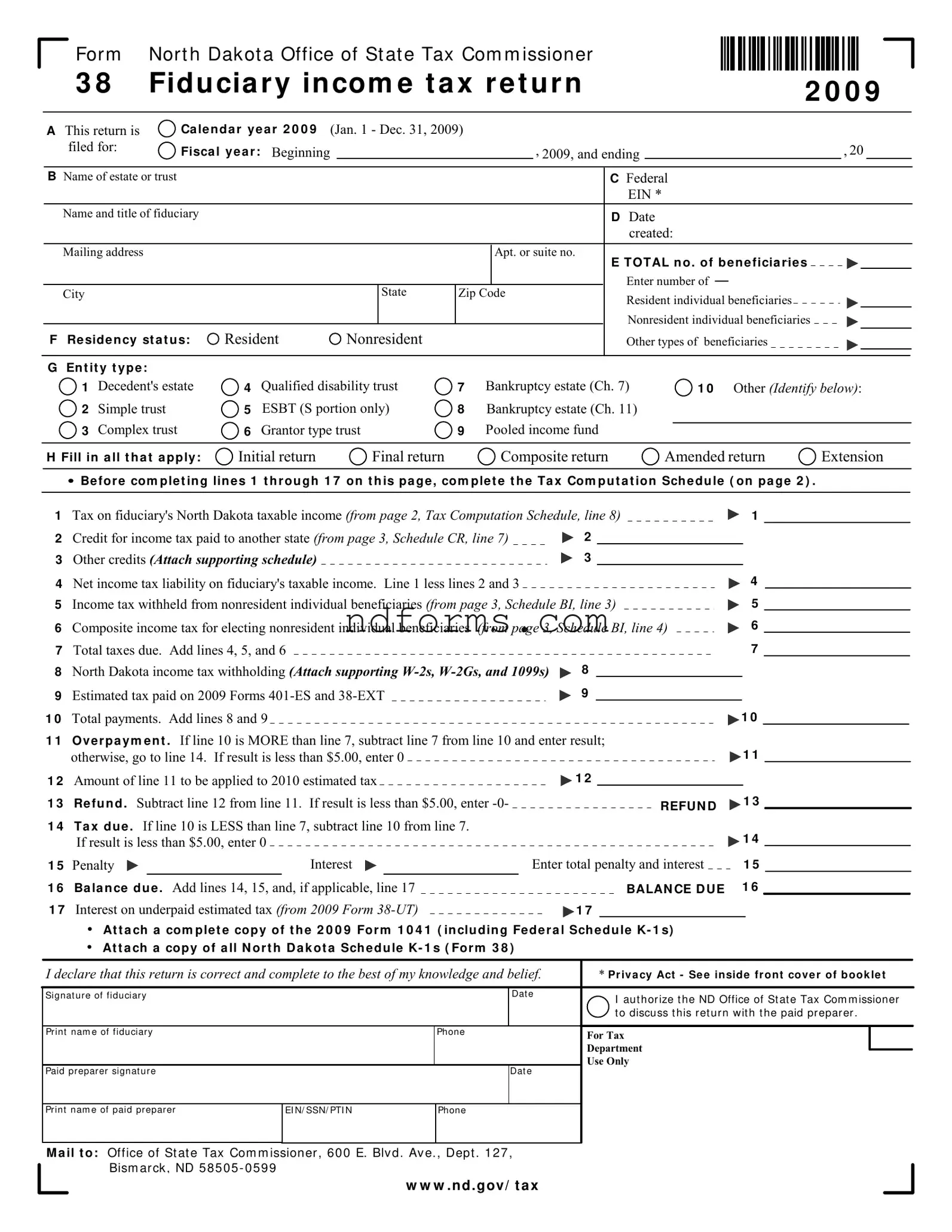

The North Dakota 38 form, officially designed for the Office of State Tax Commissioner, serves as a crucial document facilitating fiduciary income tax return filings for the calendar year 2009. Suitable for various entities such as estates, trusts (simple, complex, qualified disability trust, and grantor types), bankruptcy estates under chapters 7 and 11, and other specified entities, this form captures a wide spectrum of financial activities. Its comprehensive structure requires information concerning the estate or trust's federal Employer Identification Number (EIN), the residency status of the fiduciary (indicating whether the entity is a resident, nonresident, or falls under another category), and the type of entity filing the return. Moreover, it meticulously outlines the total number of beneficiaries, segregating them into resident individuals, nonresident individuals, and other types of beneficiaries, thus ensuring appropriate tax calculations and compliance. The form allows for various adjustments to the fiduciary's taxable income, including credits for income tax paid to other states, withholding from non-resident individual beneficiaries, and composite income tax elections, underscoring the intricate interplay between federal and state tax obligations. The precise detail requested ensures accuracy in reflecting the fiduciary's financial undertakings within North Dakota, catering to the unique tax considerations necessary for these specific entities.

Form Preview

For m Nor t h Dak ot a Office of St at e Tax Com m issioner

3 8 |

Fid u cia r y in com e t a x r e t u r n |

2 0 0 9 |

|||||

|

|

|

|

|

|||

|

|

|

|

|

|

||

A This return is |

Ca le n d a r y e a r 2 0 0 9 |

(Jan. 1 - Dec. 31, 2009) |

|

|

|

||

filed for: |

Fisca l y e a r : Beginning |

|

|

, 2009, and ending |

|

, 20 |

|

|

|

|

|

|

|||

B Name of estate or trust |

|

|

|

C Federal |

|

|

|

|

|

|

EIN * |

|

Name and title of fiduciary |

|

|

|

D Date |

|

|

|

|

|

created: |

|

Mailing address |

|

|

Apt. or suite no. |

E TOTAL n o . of b e n e ficia r i e s |

|

|

|

|

|

|

|

|

|

State |

|

Enter number of |

|

City |

|

Zip Code |

Resident individual beneficiaries |

|

|

|

|

|

|

|

|

|

|

|

|

Nonresident individual beneficiaries |

F |

Re sid e n cy st a t u s: |

Resident |

Nonresident |

|

Other types of beneficiaries |

G En t it y t y p e :

1 Decedent's estate

1 Decedent's estate

2 Simple trust

2 Simple trust  3 Complex trust

3 Complex trust

4 |

Qualified disability trust |

7 |

Bankruptcy estate (Ch. 7) |

1 0 Other (Identify below): |

5 |

ESBT (S portion only) |

8 |

Bankruptcy estate (Ch. 11) |

|

6 |

Grantor type trust |

9 |

Pooled income fund |

|

|

H Fill in a ll t h a t a pp ly : |

Initial return |

Final return |

Composite return |

Amended return |

Extension |

|||||

|

|

|

||||||||

|

Be for e com ple t in g lin e s 1 t h r ou gh 1 7 on t h is pa g e , com p le t e t h e Ta x Com p u t a t ion Sch e du le ( on p a ge 2 ) . |

|

||||||||

|

|

|

|

|

|

|

||||

1 |

Tax on fiduciary's North Dakota taxable income (from page 2, Tax Computation Schedule, line 8) |

|

1 |

|

|

|||||

2 |

Credit for income tax paid to another state (from page 3, Schedule CR, line 7) |

2 |

|

|

|

|

|

|||

3 |

Other credits (Attach supporting schedule) |

|

|

3 |

|

|

4 |

|

|

|

4 |

Net income tax liability on fiduciary's taxable income. Line 1 less lines 2 and 3 |

|

|

|

|

|

||||

5 |

Income tax withheld from nonresident individual beneficiaries (from page 3, Schedule BI, line 3) |

|

5 |

|

|

|||||

6 |

Composite income tax for electing nonresident individual beneficiaries |

(from page 3, Schedule BI, line 4) |

6 |

|

|

|||||

7 |

Total taxes due. Add lines 4, 5, and 6 |

|

|

|

|

|

7 |

|

|

|

8North Dakota income tax withholding (Attach supporting  8

8

9 Estimated tax paid on 2009 Forms |

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|||||||

1 0 |

Total payments. Add lines 8 and 9 |

|

|

|

|

|

|

|

1 0 |

|

|

|

|

|

|||||||

1 1 |

Ov e r p a y m e n t . If line 10 is MORE than line 7, subtract line 7 from line 10 and enter result; |

|

|

|

|

|

|

|

|

||||||||||||

|

otherwise, go to line 14. |

If result is less than $5.00, enter 0 |

|

|

|

1 2 |

|

|

1 1 |

|

|

|

|

|

|||||||

1 2 Amount of line 11 to be applied to 2010 estimated tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

1 3 |

Re fu n d . Subtract line 12 from line 11. If result is less than $5.00, enter |

|

|

|

REFU N D |

1 3 |

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||

1 4 |

Ta x d u e . If line 10 is LESS than line 7, subtract line 10 from line 7. |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

If result is less than $5.00, enter 0 |

|

|

|

|

|

|

|

1 4 |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

1 5 |

Penalty |

|

Interest |

|

|

Enter total penalty and interest |

1 5 |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 6 |

|

|

|

|

|

||

1 6 |

Ba la n ce d u e . Add lines 14, 15, and, if applicable, line 17 |

|

|

|

|

|

|

BALAN CE D U E |

|

|

|

|

|

||||||||

1 7 Interest on underpaid estimated tax (from 2009 Form |

|

|

|

1 7 |

|

|

|

|

|

|

|

|

|

|

|||||||

|

• |

At t a ch a com ple t e cop y of t h e 2 0 0 9 Fo r m 1 0 4 1 ( in clu din g Fe d e r a l Sch e d u le K- 1 s) |

|

|

|

|

|

|

|

|

|||||||||||

|

• |

At t a ch a cop y of a ll N or t h D a k ot a Sch e d u le K- 1 s ( For m 3 8 ) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

I declare that this return is correct and complete to the best of my knowledge and belief. |

|

|

* Pr iv a cy Act - Se e in side fr ont cov e r of b ook le t |

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Signat u r e of fidu ciar y |

|

|

|

|

Dat e |

|

|

|

I aut hor ize t he ND Office of St at e Tax Com m issioner |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

t o discu ss t his r et u r n wit h t he paid pr epar er . |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Pr int nam e of fidu ciar y |

|

|

|

Phone |

|

For Tax |

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Department |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Use Only |

|

|

|

|

|

|

|

|

||

Paid pr epar er sign at u r e |

|

|

|

|

Dat e |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pr in t n am e of paid pr epar er |

|

EI N/ SSN/ PTI N |

Phone |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

M a il t o: |

Office of St at e Tax Com m issioner , 6 0 0 E. Blv d . Av e. , Dept . 1 2 7 , |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

Bism ar ck , ND 5 8 5 0 5 - 0 5 9 9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

w w w . n d . g ov / t a x

Nor t h Dak ot a Office of St at e Tax Com m issioner

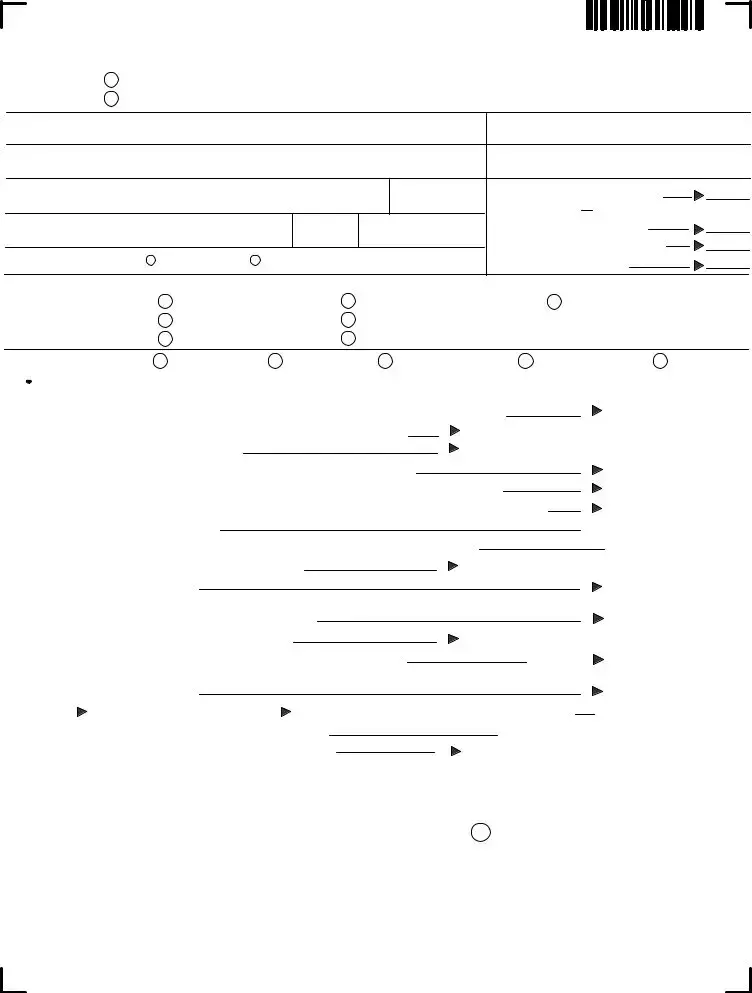

2 0 0 9 For m 3 8 , pa ge 2

Enter name of estate or trust

FEIN

Ta x Com p u t a t ion Sch e d u le : Ta x on f id u cia r y ' s t a x a b le in com e

Pa r t 1 - Ca lcu la t ion of t a x

1 Fe d e r a l t a x a b le in com e

2Additions (See instructions) (Attach supporting statement)

3Add lines 1 and 2

4a Interest from U.S. obligations

4 a

4 a

bNet

4 b

4 b

cQualified dividend exclusion

4 c

4 c

d Other subtractions (See instructions) (Attach supporting statement) |

4 d |

eTotal subtractions. Add lines 4a through 4d

5North Dakota taxable income of fiduciary. Subtract line 4e from line 3

6 Tax on amount on line 5 using the 2 0 0 9 Ta x Ra t e Sch e d u le below

•If r e side n t estate or trust, enter amount from line 6 on line 8. Do not complete lines 7a, 7b, and 7c.

•If n on r e sid e n t estate or trust, complete lines 7a, 7b, and 7c.

7 a |

Fiduciary's share of total income from Part 2, line 11, Column A, |

|

|

less the amount from Part 1, line 4a |

7 a |

b Income (loss) reportable to North Dakota from Part 2, line 11, Column B |

7 b |

|

c |

Divide line 7b by line 7a. Round to the nearest four decimal places |

7 c |

8Tax on fiduciary's North Dakota taxable income: If r e sid e n t estate or trust, enter amount from line 6. If n on r e side n t estate or trust, multiply line 6 by line 7c. Enter this amount on Form 38, page 1, line 1

2 0 0 9 |

I f t he a m oun t on lin e 5 is: |

|

|

|

|

|||

Ta x Ra t e |

Ov e r |

Bu t n ot ov e r |

Th e t a x is: |

|

|

|||

Sch e d u le |

$ |

0 |

$ 2,30 0 |

. . . . . . |

. . . . . . . . . |

. 1 . 84 % of am ount on lin e 5 |

||

|

|

2,30 0 |

5 ,350 . . . $ |

42 |

. 32 |

plus 3 . 44 % |

of t he am ou nt over |

$ 2,3 00 |

|

|

5,35 0 |

8 ,200 |

1 47 . 24 plus 3 . 81% |

of t he am oun t over |

5,35 0 |

||

|

|

8,20 0 |

11 ,15 0 |

255 |

. 83 |

plus 4 . 42 % |

of t he am ou nt over |

8,2 00 |

|

1 1,1 50 . . |

. . . . . . . . . . . . |

3 86 |

. 22 |

plus 4 . 86% |

of t he am oun t ov er |

1 1,1 50 |

|

|

|

|

|

|

|

|

|

|

1

2

3

4 e  5

5  6

6

8

Pa r t 2 - Ca lcu la t ion of fidu cia r y ' s in com e

This par t m ust be com plet ed by all est at es and t r ust s

• Re sid e n t e st a t e or t r u st : Com plet e Colum n A only .

•N on r e sid e n t e st a t e or t r u st : Com plet e Colum ns A, B, and C. See inst r uct ions for how t o com plet e Colum ns B and C.

1 |

Interest income |

1 |

2 |

Ordinary dividends |

2 |

3 |

Business income or (loss) |

3 |

4 |

Capital gain or (loss) |

4 |

5 |

Rents, royalties, partnerships, other estates and trusts, etc. |

5 |

6 |

Farm income or (loss) |

6 |

7 |

Ordinary gain or (loss) |

7 |

8 |

Other income |

8 |

9 |

Total income. Add lines 1 through 8 |

9 |

1 0 Portion of amount on line 9 distributed to beneficiaries |

1 0 |

|

1 1 Fiduciary's share of total income. Subtract line 10 from line 9 |

1 1 |

|

|

|

N on r e sid e n t e st a t e s or t r u st s on ly |

||

Colum n A |

|

|

|

|

|

Colum n B |

|

Colum n C |

|

Fe d e r a l r e t u r n |

|

N or t h D a k ot a |

|

Ot h e r St a t e s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

w w w . n d . gov / t a x

Nor t h Dak ot a Office of St at e Tax Com m issioner

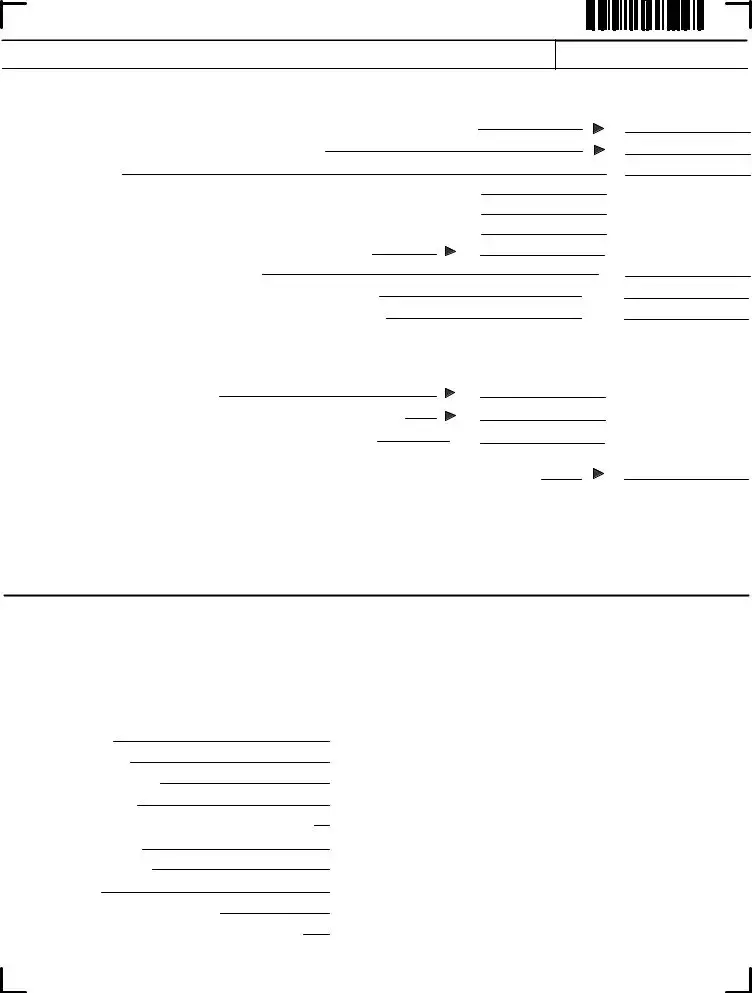

2 0 0 9 For m 3 8 , pa g e 3

Enter name of estate or trust

FEIN

|

Sch e d u le BI |

Be n e f icia r y in f or m a t ion |

|

|

|

|

|

|

|

||||||

|

|

|

|

All e st a t e s a n d t r u st s m u st |

Com plet e Colum ns 1 t hr ough 4 for EVERY beneficiar y |

|

|

|

|

|

|||||

|

|

|

|

com p le t e t h is sch e d u le |

Com plet e Colum n 5 only if beneficiar y is a nonr esident indiv idual |

|

|

|

|

||||||

|

|

|

|

|

|

|

I f applicable, com plet e Colum n 6 or Colum n 7 for nonr esident indiv idual beneficiar y only |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All Be n e ficia r ie s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Colu m n 1 |

|

|

|

Colu m n 2 |

|

Colu m n 3 |

|

|

|

|

Be n e - |

|

|

|

|

|

|

|

|

|

||||

|

|

|

Nam e and addr ess of beneficiar y |

If additional lines are needed, |

|

Social Secur it y |

|

Ty pe of ent it y |

|

||||||

|

|

ficia r y |

|

|

|

|

attach additional pages |

|

Num ber / FEI N |

|

( SEE IN ST R U CT ION S) |

|

|||

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ad dr ess |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ad d r ess |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ad dr ess |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nam e |

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ad d r ess |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

All Be n e f icia r ie s |

N on r e side n t I n div idu a l Be n e ficia r ie s On ly |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Com p le t e t h is co lu m n f o r |

I m p or t a n t : Colu m n s 5 t h r o u g h 7 a r e f or n on r e sid e n t in d iv id u a l b e n e f icia r ie s on ly . |

|

|||||||

|

|

|

|

|

|

ALL b e n e ficia r ie s |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Colu m n 4 |

Colu m n 5 |

Colu m n 6 |

|

Colu m n 7 |

|

||||

|

|

|

|

|

|

Feder al dist r ibut iv e |

Nor t h Dak ot a |

Nor t h Dak ot a |

For m |

|

Nor t h Dak ot a |

|

|||

|

|

|

Be n e ficia r y |

|

shar e of incom e ( loss) |

dist r ibut iv e shar e of |

incom e t ax |

PWA |

com posit e incom e t ax |

|

|||||

|

|

|

|

|

|

incom e ( loss) |

w it hheld |

|

|

( 4 . 8 6 % ) |

|

||||

|

|

|

|

|

|

|

|

|

( 4 . 8 6 % ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

1Total for Column 4 . . . . . . 1

2Total for Column 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3Total for Column 6. Enter this amount on Form 38, page 1, line 5 . . . . . . . . . . . . . . . . 3

4Total for Column 7. Enter this amount on Form 38, page 1, line 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Sch e d u le CR |

Cr e d it f or in com e t a x p a id t o a n ot h e r st a t e ( r e side n t e st a t e or t r u st on ly ) |

1 |

Fiduciary's share of total income. Enter amount from Tax Computation Schedule, Part 2, line 11, Column A |

||

2 |

Portion of amount on line 1 that has its source in the other state (See instructions) |

|

|

3 |

Credit ratio. Divide line 2 by line 1 and round to the nearest four decimal places |

3 |

|

4Tax on fiduciary's North Dakota taxable income from Form 38, page 1, line 1

5 |

Multiply line 3 by line 4 |

6 |

Amount of income tax paid to the other state (See instructions) |

7Credit for income tax paid to another state. Enter lesser of line 5 or line 6. Enter this amount on page 1, line 2

I m por t a n t : At t a ch a co py of t h e in com e t a x r e t u r n file d w it h t h e ot h e r st a t e

1

2

4

5

6

7

w w w . n d . g ov / t a x

File Attributes

| Fact Name | Description |

|---|---|

| Filing Purpose | The North Dakota 38 form serves as the fiduciary income tax return for the state. |

| Eligible Entities | Included entities for this form are decedent's estates, simple trusts, complex trusts, qualified disability trusts, grantor type trusts, and bankruptcy estates among others. |

| Residency Status | Indicates whether the estate or trust is resident, nonresident, or falls under another category within North Dakota. |

| Beneficiary Information | Details pertaining to both resident and nonresident individual beneficiaries must be provided, including the number of each type. |

| Tax Calculation | Tax is calculated on the fiduciary's North Dakota taxable income with provisions for credits, such as income tax paid to another state and other applicable credits. |

| Governing Law | These provisions and requirements are pursuant to North Dakota state tax law, specifically tailored for fiduciary income tax return processing and obligations. |

How to Write North Dakota 38

Upon receiving the North Dakota 38 Fiduciary Income Tax Return for the year 2009, individuals responsible for handling the finances of estates or trusts face a structured procedure to correctly report income, deductions, and taxes due. This process, vital for compliance with state tax laws, ensures the financial obligations are met in detail. The form is multifaceted, designed to capture various aspects of fiduciary financial activity within the taxable year or fiscal period stipulated.

- Identify the type of entity filing the return by selecting the appropriate box in section G, considering options from decedent's estate to various forms of trusts and bankruptcy estates.

- Mark the box corresponding to the residency status of the estate or trust in section F, choosing from 'Resident', 'Nonresident', or 'Other'.

- Complete section A by indicating whether the form is filed for the calendar year (January 1 - December 31, 2009) or a different fiscal year by specifying the beginning and end dates.

- Provide the name of the estate or trust, along with the federal Employer Identification Number (EIN), in section B.

- Enter the name and title of the fiduciary, the date the trust was created, and the complete mailing address including the apt or suite number, city, state, and zip code in sections C and D.

- Input the total number of beneficiaries, including both resident and nonresident individuals, as well as other types of beneficiaries, in section E.

- Before completing the lines on the form's first page, fill out the Tax Computation Schedule on page 2 to calculate the tax on the fiduciary's North Dakota taxable income.

- Enter the calculated tax from the Tax Computation Schedule into line 1 of the form.

- Complete the schedules for credit for income tax paid to another state (if applicable), as well as the beneficiary information and the calculation of tax withholding for nonresident individual beneficiaries, then input these figures into the corresponding lines on the form.

- If overpayment is determined on line 11, decide the amount to be applied to next year's estimated tax and the refund amount. Conversely, if the result shows tax due, calculate any penalties, interest, and sum up the total balance due.

- Attach a complete copy of the 2009 Form 1041, including Federal Schedule K-1s, and all North Dakota Schedule K-1s (Form 38).

- Review the form for accuracy, then sign and date the document in the designated section at the bottom. If prepared by someone other than the fiduciary, the preparer also needs to sign and provide contact information.

- Mail the completed form and any additional required documents to the Office of the State Tax Commissioner at the address provided in the form instructions.

By meticulously following these steps, fiduciaries can effectively fulfill their legal obligation to report income and calculate taxes owed by estates or trusts under their management, ensuring that all financial activities are conducted within the framework of North Dakota's tax laws.

Your Questions, Answered

- What is Form North Dakota 38?

- Who needs to file Form North Dakota 38?

- What are the key sections of Form North Dakota 38?

- Identification of the estate or trust and the fiduciary responsible for it.

- Details about the taxable year and residency status of the entity.

- A tax computation schedule to calculate the tax on the fiduciary's North Dakota taxable income.

- Sections for claiming credits for income tax paid to other states, and for income tax withheld from nonresident individual beneficiaries.

- Information on estimated tax paid and the total payments versus the total taxes due.

- How does one determine the residency status for Form North Dakota 38 filing?

Form North Dakota 38 is a fiduciary income tax return used by estates and trusts for reporting income, gains, losses, deductions, and credits for the tax year. It is specifically designed for fiduciaries to fulfill their tax obligations to the North Dakota Office of State Tax Commissioner. The form covers various types of entities, including decedent's estates, simple trusts, complex trusts, and others, specifying their income and taxation details within the state of North Dakota.

Form North Dakota 38 must be filed by the fiduciary (trustee or executor) of a resident or nonresident estate or trust that has income from North Dakota sources or is required to report and pay income tax to North Dakota. This includes resident estates or trusts regardless of where their income comes from and nonresident estates or trusts that earn income from sources within North Dakota.

Key sections of Form North Dakota 38 include:

The residency status for file Form North Dakota 38 depends on where the estate or trust is administered and the source of its income. A resident estate or trust is one that is administered in North Dakota or one that receives income from North Dakota sources regardless of the administration location. A nonresident estate or trust, on the other hand, is administered outside of North Dakota and may have income from sources within North Dakota, requiring them to file Form 38 if they meet certain income thresholds or have tax obligations in North Dakota.

Common mistakes

Filling out tax forms can be daunting, and the North Dakota 38 Fiduciary Income Tax Return is no exception. Here are four common mistakes people make which can delay processing time or even affect the amount of tax owed.

- Incorrect Residency Status: The North Dakota 38 form requires the filer to denote the residency status of the estate or trust. Confusion often arises between 'Resident,' 'Nonresident,' and 'Other' categories. This mistake can lead to miscalculations in the amount of tax due or refunds. Ensuring accuracy here is crucial because it dictates which portions of the income are subject to North Dakota state taxes.

- Not Attaching Required Documents: Another common pitfall is failing to attach all required documents, such as a complete copy of the 2009 Form 1041 and all North Dakota K-1 forms (Form 38). These documents provide necessary details to accurately assess the fiduciary's taxable income and verify the information reported on the return. Omitting these could result in delays or an incorrect assessment of taxes.

- Inaccurate Beneficiary Information: Schedule BI of the form asks for detailed information about each beneficiary, including nonresident individuals. Misreporting or neglecting to provide complete details in this section, such as incorrect Social Security Numbers or addresses, can lead to problems in the allocation of income or tax withholdings for beneficiaries, potentially affecting their own tax liabilities and the overall accuracy of the fiduciary return.

- Miscalculating Credits and Deductions: When completing lines 1 through 17, it's crucial to accurately transfer amounts from the Tax Computation Schedule and other supporting schedules, like Schedule CR for credits for income tax paid to another state. Errors in this section can significantly impact the fiduciary's net income tax liability, the refund amount, or the balance due. Overlooking or double-counting credits and deductions is a mistake that can lead to discrepancies and potential audits.

Avoiding these errors requires careful review, attention to detail, and adherence to the instructions provided by the North Dakota Office of State Tax Commissioner. When in doubt, consulting with a tax professional can provide clarity and ensure that your fiduciary income tax return is accurately prepared. The complexity of fiduciary tax responsibilities means that getting it right the first time can save significant time and effort in amendments and communications with the tax authorities.

Documents used along the form

In the realm of estate and fiduciary income tax preparation, the North Dakota Form 38 is crucial for reporting income, deductions, and taxes owed by estates or trusts. However, it's important to understand that this form does not stand alone. A comprehensive approach typically involves several other forms and documents to ensure compliance with tax regulations and to fully capture the financial activities of the entity in question. The description of these additional documents below will help in painting a more complete picture.

- Schedule K-1 (Form 1041): This form details the share of income, deductions, and credits allocated to each beneficiary of the estate or trust. It allows beneficiaries to correctly report their share of the entity's income on their personal tax returns.

- Form 1041: The U.S. Income Tax Return for Estates and Trusts is used to report the income, gains, losses, deductions, and credits of the estate or trust. It's the federal counterpart to the North Dakota Form 38, ensuring that the information provided aligns with federal tax filings.

- Form 38-UT: This form calculates the interest on underpaid estimated tax by estates and trusts in North Dakota. If the payments made during the year did not meet certain thresholds, this form helps compute what additional interest may be due.

- Schedule CR: Specifically for estates or trusts that paid income tax to another state, this schedule allows for a credit on the North Dakota return, preventing double taxation of the same income. It requires detailed information about the taxes paid to other states.

Together, these forms and documents work in harmony with Form 38 to provide a full account of an estate or trust's financial activities and tax obligations. Navigating through them requires meticulous attention to detail and an understanding of tax laws that apply to fiduciary entities. Proper completion and submission of these forms ensure compliance with tax regulations, avoiding penalties and fostering a smoother process for beneficiaries and fiduciaries alike.

Similar forms

The North Dakota 38 form is similar to the Form 1041, commonly known as the U.S. Income Tax Return for Estates and Trusts. Both documents are designed to report income, deductions, and credits of estates and trusts. The similarity extends to their structure, as they both require detailed information about the income sources of the fiduciary entity, deductions allowed under the law, and applicable credits that reduce the taxable income. Notably, each form mandates the reporting of distributions to beneficiaries, adjusting for any taxable amounts that may affect the beneficiaries' individual tax obligations. The main difference lies in their jurisdictional application; Form 1041 is used at the federal level, while the North Dakota 38 form applies to fiduciary entities operating within the state of North Dakota.

Another document similar to the North Dakota 38 form is the Schedule K-1 (Form 1041), which is used for beneficiaries of estates and trusts to report their share of the entity's income, credits, deductions, etc., on their own personal tax returns. Like the North Dakota 38 form, Schedule K-1 focuses on the allocation of income and deductions to the appropriate beneficiaries. However, while the North Dakota 38 form is filled out by the fiduciary to report the entity's overall tax responsibility to the state, Schedule K-1 is a federal form used to pass on information to individual beneficiaries about their portion of the entity's financial activities that they will need to include on their personal tax returns. This ensures transparency and aids in the accurate reporting of income and the calculation of tax liabilities for beneficiaries.

Dos and Don'ts

When completing the North Dakota Form 38 for fiduciary income tax returns, there are specific steps you should follow to ensure accuracy and compliance with state tax regulations. Below are lists of do's and don'ts to guide you through the process.

Do:

- Read the instructions provided by the North Dakota Office of State Tax Commissioner carefully before you start.

- Ensure that the form is for the correct tax year and you're using the form designated for a fiduciary income tax return.

- Complete every required section according to the instructions, using information from the federal Form 1041 and other relevant documents.

- Attach a complete copy of the 2009 Form 1041, including Federal Schedule K-1s, as instructed.

- Provide the correct Federal EIN (Employer Identification Number) of the estate or trust.

- Indicate the correct residency and entity type for the estate or trust as these details affect tax computation.

- If applicable, accurately report income tax withheld and composite income tax for nonresident individual beneficiaries.

- Take advantage of any credits for income tax paid to another state, ensuring all calculations and documentation are correct.

- Review the entire form for accuracy and completeness before signing.

- Make sure to sign and date the return, and, if you’re using a paid preparer, ensure they also sign and include their information.

Don't:

- Leave any required fields blank. If something does not apply, enter “N/A” or “0” as dictated by the form instructions.

- Mistake the calendar year for the fiscal year if filing for a period different than January 1 - December 31, 2009.

- Forget to attach all necessary schedules, including North Dakota Schedule K-1s and supporting documentation for credits and deductions.

- Enter incorrect beneficiary information on Schedule BI. Ensure all details, such as names, addresses, and Social Security or EIN numbers, are accurate.

- Ignore instructions regarding attachments for credits for income tax paid to another state. This includes failing to attach a copy of the income tax return filed with the other state.

- Misinterpret the tax rate schedules and calculation instructions, leading to incorrect tax liability.

- Estimate figures or leave them to be filled in later. Use actual figures from documentation and worksheets.

- Omit the date or signature, as an unsigned return is considered not filed.

- Fail to authorize the ND Office of State Tax Commissioner to discuss the return with the paid preparer, if applicable.

- Delay in mailing the completed form to the address provided by the due date, which may result in penalties and interest.

By adhering to these guidelines, you will help ensure that the fiduciary income tax return for the estate or trust is properly and accurately filed.

Misconceptions

Misconceptions often arise regarding the complexity and specifics of tax forms, including the North Dakota Form 38, which deals with fiduciary income tax returns. Understanding the form's requirements can demystify the process and enable better compliance. Here are seven common misconceptions about the North Dakota 38 Form:

The form is only for trusts and does not concern estates. In reality, Form 38 is designed for both trusts and estates. The form encompasses various entity types, including decedent's estates, simple trusts, complex trusts, and more, underscoring the form's broader applicability than often perceived.

Nonresident entities do not need to file this form. Quite the opposite, both resident and nonresident estates or trusts with North Dakota taxable income are required to file. The form has provisions to calculate tax liabilities based on residency status, ensuring that nonresident entities are also accounted for.

Form 38 is strictly for annual tax filing. While it does serve the annual tax filing requirements, Form 38 is versatile, covering initial, final, composite, and amended returns as well. This adaptability makes it a critical component of fiduciary tax compliance through diverse scenarios.

All beneficiaries' information is processed the same. The form differentiates between resident and nonresident individual beneficiaries, especially in portions related to income tax withholding and composite income tax. Such distinctions are crucial for accurate tax assessment and compliance.

Credits for income tax paid to another state are straightforward. While the form does allow fiduciaries to claim a credit for tax paid to other states, calculation of this credit involves a nuanced process. It requires understanding the portion of income sourced from other states and applying a specific credit ratio, highlighting the need for meticulous attention to the instructions.

Submission without attachments is sufficient. In truth, alongside the completed Form 38, fiduciaries must attach a copy of the Federal Form 1041 and North Dakota Schedule K-1s. These documents are critical for providing a comprehensive overview of the estate or trust's income and tax liabilities.

Information about the fiduciary and preparer is optional. The authorization section of the form is a testament to the importance of fiduciary and preparer information. It not only facilitates direct communication between the tax authorities and the representatives but also underscores accountability and the legal declaration of the form's accuracy.

Understanding the North Dakota 38 Form in depth clarifies the obligations and opportunities for fiduciaries managing estate or trust tax filings. Dispelling these misconceptions can lead to smoother, more accurate compliance with state tax laws.

Key takeaways

Understanding how to accurately complete the North Dakota Form 38, or Fiduciary Income Tax Return, is essential for those managing estates or trusts within the state. Here are key takeaways to ensure the form is filled out correctly and all relevant data is properly reported.

- The North Dakota Form 38 is designated for the calendar year 2009, covering January 1 through December 31, 2009, but it is also applicable for fiscal years that begin and end in specified dates within 2009.

- Identification details such as the name of the estate or trust, the federal EIN, and the fiduciary's contact information are crucial for proper filing and should be entered accurately in the designated sections.

- It's important to specify the residency status of the estate or trust, as this determines the tax liabilities and benefits available. The form accommodates resident, nonresident, and other types of beneficiaries.

- The entity type of the fiduciary, whether it's a decedent's estate, a simple or complex trust, or another specified type, must be clearly identified for tax purposes.

- Filers must indicate whether the return is an initial, final, composite, or amended return, and if an extension has been granted or applied for.

- Before calculating the tax owed, one must complete the Tax Computation Schedule on page 2, which helps determine the fiduciary's North Dakota taxable income.

- For estates and trusts with nonresident beneficiaries, withholding taxes and composite income taxes may apply. These amounts must be calculated and reported on the form to comply with state regulations.

- Supporting documentation, including a copy of the federal return (Form 1041 including Federal Schedule K-1s) and all North Dakota Schedule K-1s, must be attached, ensuring that the state tax authorities have all the information needed to assess the fiduciary's tax liability accurately.

By keeping these key points in mind, estates and trusts can navigate the complexities of North Dakota's fiduciary income tax requirements more effectively. Fiduciaries are encouraged to review the complete form and instructions or consult a tax professional to ensure compliance and avoid potential penalties.

Browse Popular Documents

North Dakota Filing Requirements - The layout of Form 306 includes checkboxes and fields for various updates and changes, making it easier for taxpayers to report accurate information.

North Dakota Nonresident Filing Requirements - The ND-1 form is used by individuals to file their income tax return with the North Dakota Office of State Tax Commissioner.

North Dakota Tax Rate - Steps to calculate the total amount due with the return, consolidating various tax obligations.