Printable North Dakota 58 Template

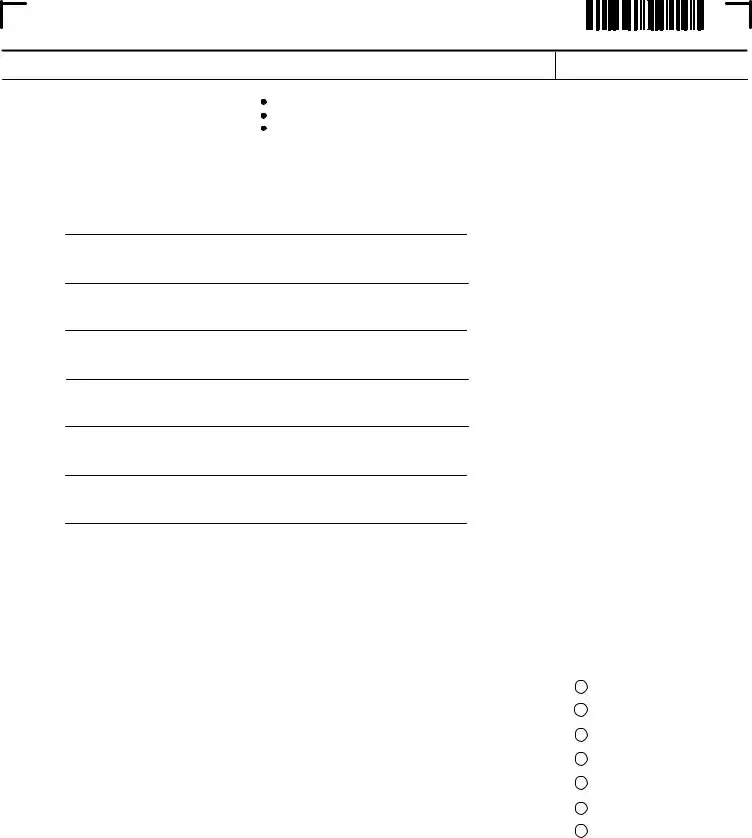

Navigating the complexities of tax obligations for partnerships in North Dakota can feel like a daunting task, but understanding the application of the North Dakota 58 form is a crucial aspect of compliance. Issued by the North Dakota Office of State Tax Commissioner, the 2010 iteration of Form 58 specifically caters to partnerships, demanding detailed reporting through Schedule KP for every partner involved. The form meticulously requires partnerships to provide comprehensive details including, but not limited to, the name and address of each partner, their Social Security or Federal Employer Identification Number (FEIN), the type of entity they are, and their respective ownership percentages. Additionally, the form takes a deeper dive when it comes to nonresident individual partners by mandating the completion of extra columns dedicated to their federal distributive share of income or loss and specific North Dakota tax considerations. These include the North Dakota distributive share of income (loss) and the actionable items pertaining to North Dakota’s unique approach to income tax withholding for nonresident individuals, distinguishing between a general withholding requirement and the option for a composite income tax payment. This level of detail embodies the state's effort to ensure that all income generated within its borders by partnerships is accurately reported and taxed accordingly, which underscores the importance of mastering the intricacies of Form 58 for entities engaged in partnership business within North Dakota.

Form Preview

North Dakota Office of State Tax Commissioner

2010 Form 58, page 5

Enter name of partnership

FEIN

|

Schedule KP |

Partner information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

All partnerships must |

Complete Columns 1 through 5 for EVERY partner |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

complete this schedule |

Complete Column 6 if partner is a nonresident individual |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

If applicable, complete Column 7 or Column 8 for a nonresident individual partner only |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All Partners |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Column 1 |

|

|

|

|

|

Column 2 |

|

Column 3 |

Column 4 |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name and address of partner |

|

|

|

If additional lines are needed, |

Social Security |

|

Type of entity |

Ownership |

|||||||||

|

|

Partner |

|

|

|

|

|

|

attach additional pages |

Number/FEIN |

|

(See pg. 7 of instr.) |

% |

|

|

|||||||

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E |

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

F |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All Partners |

|

|

|

Nonresident Individual Partners Only |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Complete this column for |

|

Important: Columns 6 through 8 are for nonresident individual partners only. |

|||||||||||||

|

|

|

|

|

|

|

ALL partners |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Column 5 |

|

|

|

Column 6 |

|

Column 7 |

|

|

Column 8 |

||||||

|

|

|

|

|

|

|

Federal distributive |

|

|

North Dakota |

|

North Dakota |

|

Form |

North Dakota |

|||||||

|

|

|

|

|

Partner |

share of income (loss) |

|

distributive share of |

|

income tax |

|

PWA |

composite income tax |

|||||||||

|

|

|

|

|

|

|

|

|

income (loss) |

|

withheld |

|

|

|

(4.86%) |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(4.86%) |

|

|

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

F |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

1 Total for COLUMN 5 . . . . . . 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

2 Total for COLUMN 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

3 Total for COLUMN 7. Enter this amount on Form 58, page 1, line 1 . . . . . . . . . . . . . . . . 3 |

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

4 Total for COLUMN 8. Enter this amount on Form 58, page 1, line 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 |

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

www.nd.gov/tax |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

File Attributes

| Fact Number | Description |

|---|---|

| 1 | The form is issued by the North Dakota Office of State Tax Commissioner. |

| 2 | Form 58 is designed for use in the year 2010. |

| 3 | It is specifically intended for partnerships to report partner information. |

| 4 | Partnerships must complete Schedule KP as part of Form 58. |

| 5 | The form requires details for every partner, including name, address, Social Security Number/Federal Employer Identification Number (SSN/FEIN), type of entity, and ownership percentage. |

| 6 | Nonresident individual partners have additional requirements for columns 6 through 8. |

| 7 | Column 6 is for reporting the North Dakota distributive share of income (loss) for nonresident individual partners. |

| 8 | Columns 7 and 8 involve North Dakota income tax withheld and PWA composite income tax, respectively, both at a rate of 4.86%. |

| 9 | All partnership types are required to fill out columns 1 through 5 for every partner. |

| 10 | The governing law for Form 58 and its associated requirements is the tax code of North Dakota. |

How to Write North Dakota 58

Filling out the North Dakota Form 58 is a step crucial for partnerships operating within the state. This document, required by the Office of State Tax Commissioner, ensures that the appropriate income distributions are reported accurately for tax purposes. Given the complexity of tax documentation, careful attention to detail is paramount to avoid any potential discrepancies. The process demands a systematic approach, encompassing the entry of partner details to specific financial distributions. The following sequence of steps simplifies this process, guiding through the necessary fields to ensure complete and accurate form submission.

- Begin by entering the name of the partnership and its Federal Employer Identification Number (FEIN) at the designated top section of the form.

- Under Schedule KP - Partner Information, list each partner’s information. Start with the Name and Address of Partner (Column 1). Include the state and zip code for each partner listed.

- Proceed to fill out each partner’s Social Security Number (SSN) or FEIN (Column 2), depending on the type of entity.

- Identify the Type of Entity (Column 3) for each partner, referring to page 7 of the instructions for guidance if necessary.

- Enter the Ownership Percentage (Column 4) for every partner, ensuring accuracy as it impacts the allocation of income or loss.

- For ALL partners, input the Federal distributive share of income (loss) (Column 5).

- If the partner is a nonresident individual, fill out the North Dakota distributive share of income (loss) (Column 6).

- For nonresident individual partners, if applicable, enter the North Dakota income tax withheld (4.86%) (Column 7).

- Similarly, for nonresident individuals, complete the Form North Dakota PWA composite income tax (4.86%) (Column 8), if it applies.

- Review the form to ensure that all details have been accurately filled. Attach additional pages if more space is required for partner details.

- Total the amounts in Columns 5 through 8 at the bottom of their respective columns and report these totals as instructed.

- Once fully completed, refer to the totals derived from Columns 7 and 8 and enter these on Form 58, page 1, lines 1 and 2, respectively.

After completing the form with the required information, the next steps include verifying the accuracy of all entered data, signing the document where necessary, and submitting it to the North Dakota Office of State Tax Commissioner by the due date. Timely and accurate submission of Form 58 plays a crucial role in ensuring the partnership’s compliance with North Dakota’s tax regulations, ultimately facilitating a smoother tax processing and avoiding possible penalties for errors or late submissions.

Your Questions, Answered

FAQs about North Dakota Form 58

What is North Dakota Form 58?

North Dakota Form 58 is a document created by the North Dakota Office of State Tax Commissioner. It’s designed for partnerships to report and provide detailed information about their partners. This includes personal info, the type of entity each partner is, their percent of ownership, and specific financial details for both resident and nonresident partners.

Who needs to fill out Form 58?

Every partnership operating within North Dakota must complete Form 58. This requirement applies regardless of whether the partners are North Dakota residents or nonresidents. By accurately completing this form, partnerships ensure compliance with state tax obligations.

What information is required on Form 58?

Partnerships must provide a comprehensive list of details for each partner. This includes:

- The partner's name and address

- The partner's Social Security Number (SSN) or Federal Employer Identification Number (FEIN)

- The type of entity of each partner

- Percentage of ownership for each partner

- Specific income or loss distribution details, particularly for nonresident partners

For nonresident individual partners, additional columns related to North Dakota income and withheld taxes must be completed.

How do partnerships handle additional partners?

If a partnership has more partners than there are lines provided on the main form, additional pages should be attached to include everyone. It’s important to ensure that the information for each partner is reported fully and accurately, following the format laid out in the original document.

Are there special considerations for nonresident partners?

Yes. For nonresident partners, the partnership must complete additional columns related to the distributive share of North Dakota income or loss and any North Dakota income taxes that were withheld. This information is crucial for ensuring that nonresident partners meet their state tax obligations appropriately.

Where can one find more information or assistance with Form 58?

The North Dakota Office of State Tax Commissioner’s website is the best resource for finding more details on Form 58. They provide guidelines, instructions, and contact information for any questions or help required. Additionally, consulting with a tax professional knowledgeable about North Dakota state tax laws can be very beneficial.

Common mistakes

Filling out the North Dakota Form 58 requires attention to detail. It's easy to make mistakes that can lead to delays or issues with the state tax return. Here are ten common errors people tend to make:

- Incorrect Names and Addresses: Filling in incorrect or incomplete names and addresses in Column 1 is a common mistake. Each partner's information must match official records.

- Social Security Number (SSN) or FEIN Issues: Misstating the SSN or FEIN in Column 2 can lead to processing errors or mismatches in the tax system.

- Entity Type Confusion: In Column 3, partners sometimes incorrectly classify the type of entity. It's important to correctly identify the type, as this can affect tax liabilities and obligations.

- Ownership Percentage Errors: Column 4 requires accurate reporting of ownership percentages. Inaccuracies here could lead to incorrect calculation of taxes owed.

- Omitting Federal Distributive Share Information: Column 5 is crucial for calculating the federal distributive share of income (or loss). Omitting or inaccurately reporting this figure can alter tax responsibilities.

- Failing to Complete Nonresident Sections: Nonresident individual partners must have Column 6 filled. Neglecting to complete this section means not complying with state requirements for nonresidents.

- Inaccurate North Dakota Shares: Columns 7 and 8 deal with North Dakota distributive share and withheld tax, respectively. Mistakes here could affect the partner’s tax filings and lead to unpaid taxes.

- Forgetting Additional Pages: When partnerships have more partners than can fit on the provided form, additional pages are necessary. Failing to attach these can result in incomplete filings.

- Incomplete Totals: Not totaling Columns 5 through 8 correctly can impact the calculation on the main tax return form, potentially resulting in an underpayment or overpayment of tax.

- Incorrect Form Versions: Using an outdated version of Form 58 can lead to compliance issues, as tax laws and requirements may have changed.

It's essential to review Form 58 carefully before submitting it. Ensuring all information is accurate and complete can save time and prevent issues with the North Dakota Office of State Tax Commissioner. When in doubt, consulting the instructions or a tax professional can help clarify any confusion. Keeping records updated and double-checking the form can go a long way in making the tax filing process smoother.

Documents used along the form

When managing tax and legal responsibilities in North Dakota, particularly for partnerships, the Form 58 often stands at the center of necessary documentation. However, it functions within a broader ecosystem of forms and documents that serve specific purposes, ranging from establishing entity structures to fulfilling state tax obligations. Understanding these documents helps in comprehensively managing a partnership’s legal and tax considerations.

- Form 40PT: This form is designated for the reporting of partnership income tax. It is a critical document that complements Form 58, providing detailed information on the income generated and taxes owed by the partnership as an entity.

- Form 60: Used by nonresident partners, this form helps in declaring and settling individual income tax responsibilities to North Dakota, especially in cases where income has been earned within the state.

- Form ND-EZ: A simplification for individual income tax returns, this form is relevant for residents with straightforward tax situations, potentially including resident partners in a partnership.

- Schedule K-1 (Form 1065): This federal document outlines an individual partner’s share of partnership income, deductions, credits, etc., vital for both federal and state tax preparation.

- Form PTE: Focused on S Corporations and Partnerships, this form is used for making estimated tax payments. It supports proactive tax management throughout the fiscal year.

- Form SFN 58702: Required for registering a partnership in North Dakota, this form establishes the legal presence of a partnership, enabling it to conduct business within the state.

- Annual Report: While not a standardized form, partnerships in North Dakota must file an annual report with the Secretary of State, detailing key aspects of the partnership’s status and activities.

- Zoning Permits or Land Use Documents: Depending on the location and nature of the partnership’s operations, local zoning permits may be necessary. These documents ensure compliance with municipal regulations regarding land use and operations.

- Employer Identification Number (EIN) Application (Form SS-4): Critical for tax identification purposes, this federal form is necessary for any partnership operating as a distinct entity, particularly in relation to hiring employees and opening bank accounts.

Together, these documents form the backbone of a partnership's administrative, legal, and tax framework in North Dakota. Keeping accurate and up-to-date records across these forms not only facilitates compliance with state and federal regulations but also aids in the smooth operational management of the partnership. Whether initiating a new partnership or managing ongoing requirements, these forms provide the structured pathways necessary for legal and fiscal responsibility.

Similar forms

The North Dakota 58 form is similar to several other documents used for tax and financial reporting in relation to partnerships and their members. These forms share a focus on providing detailed information about the identity and financial status of partners, as well as the distribution of income or losses within a partnership. While each form has its distinct purposes and requirements, the underlying goal is to ensure transparency and compliance with tax laws.

One document similar to the North Dakota 58 form is the IRS Schedule K-1 (Form 1065). It serves as a tool for reporting an individual partner's share of a partnership's earnings, deductions, credits, etc., to the IRS. Just like the North Dakota 58 form requires the listing of partners and their shares of income or loss, Schedule K-1 emphasizes the individualized distribution of the partnership's financial outcomes. Both documents necessitate detailed accounting of income distributions and are pivotal for both the partnership and the partners to fulfill their tax obligations appropriately.

Another document resembling the North Dakota 58 form is the Form 8804, or the Annual Return for Partnership Withholding Tax (Section 1446). This form is utilized to report the withholding tax on foreign partners' share of effectively connected income in a partnership conducting business in the United States. Much like the sections within the North Dakota 58 form that deal with nonresident individual partners, Form 8804 focuses on the tax obligations incurred from income distributions to partners who are not U.S. residents. The alignment between these forms highlights the regulation around cross-border income and the taxation frameworks designed to account for the global nature of modern business partnerships.

Additionally, the State-specific Partner’s Share of Income, Deductions, Credits, etc. forms, which can vary by state, are comparable to the North Dakota 58 form. These forms also focus on the allocation of income, deductions, and credits among partners within a given state's jurisdiction. Although the specific details and requirements can differ from one state to another, the core concept of distributing tax responsibilities based on partnership agreements reflects the North Dakota 58 form’s objectives. These similarities underscore the universal need for transparent reporting in the partnership taxation landscape, facilitating a standardized approach towards managing and disclosing partnership financial activities across different states.

Dos and Don'ts

When completing the North Dakota Form 58, it's essential to pay careful attention to detail. Following are ten do's and don'ts to guide you through the process:

- Do:

- Ensure that you enter the correct Partnership Federal Employer Identification Number (FEIN) at the top of the form.

- Complete columns 1 through 5 for every partner, as all partnership information is mandatory.

- For nonresident individual partners, make sure to fill in Column 6 with the correct information.

- If applicable, accurately complete Column 7 or Column 8 for nonresident individual partners.

- Attach additional pages if you have more partners than the form can accommodate, ensuring that the format matches that of the form.

- Verify all the percentages of ownership are correctly calculated and entered in the designated column.

- Double-check the social security numbers/FEINs provided for accuracy.

- Carefully review the total distributive share of income (loss) for accuracy before submission.

- Ensure the form is signed and dated.

- Don't:

- Don't leave any fields blank. If a section does not apply, indicate with "N/A" or "0", as appropriate.

- Don't forget to complete the special columns (6 through 8) specifically for nonresident individual partners.

- Avoid making errors in the partners' names and addresses—these should match official documents.

- Don't miss attaching additional pages if more space is needed, but ensure they're correctly formatted and labeled.

- Never guess information. Verify all entries for correctness before submission.

- Avoid the use of corrections fluid or tape; if you make an error, it's best to start with a clean form.

- Don't overlook the instructions page, which may have valuable guidance on filling out the form accurately.

- Do not submit the form without checking that all applicable columns for nonresident individuals have been completed.

- Avoid late submission to prevent possible penalties.

Misconceptions

When it comes to understanding and completing the North Dakota 58 form, many misconceptions exist. It's crucial to address these misunderstandings to ensure accurate and timely submissions, which support compliance with state tax regulations. Here are eight common misconceptions about the North Dakota 58 form:

- Misconception 1: All partners, regardless of their residency, must complete columns 6 through 8. In reality, columns 6 through 8 are intended only for nonresident individual partners. This differentiation ensures that only relevant information pertaining to nonresident partners' income and withholding is provided.

- Misconception 2: The North Dakota 58 form is required for all businesses operating within the state. However, this form is specifically designed for partnerships, detailing income distribution and tax withholding for partners. It is not a general business tax form.

- Misconception 3: There's no need to attach additional pages if the provided space is insufficient. This is incorrect, as partnerships with more partners than the form can accommodate should attach additional pages, ensuring that every partner's information is fully reported.

- Misconception 4: Personal social security numbers (SSNs) or federal employer identification numbers (FEINs) are optional. In truth, providing the SSN or FEIN for each partner is mandatory, enabling accurate identification and tax processing for every individual and entity involved.

- Misconception 5: The type of entity column is not significant. Contrary to this belief, correctly identifying the type of entity for each partner is crucial, as it affects tax treatment and obligations under North Dakota law.

- Misconception 6: The ownership percentage is not important for the form's completion. This information is vital as it determines the proportionate share of income or loss allocated to each partner, directly impacting their tax liability.

- Misconception 7: Nonresident individual partners are exempt from North Dakota income tax withholding. Nonetheless, nonresident individuals may have North Dakota tax withheld at a rate of 4.86%, as specified in columns 7 and 8, ensuring they meet their tax obligations to the state.

- Misconception 8: The form does not need to be updated for changes in partnership or partner information after initial submission. It's imperative to keep the information up to date, as changes in partnership composition or partner details can affect tax responsibilities and entitlements.

By clarifying these misconceptions, partnerships can better navigate the complexities of tax reporting and compliance, fostering a smoother relationship with tax authorities and enhancing the accuracy of their financial and tax records.

Key takeaways

Filling out the North Dakota 58 form is a critical procedure for partnerships operating within the state. It is designed to ensure that all income, deductions, and tax withholdings are accurately reported to the North Dakota Office of State Tax Commissioner. Below are six key takeaways to guide you through the process:

- Partnership Information: The form requires detailed information about the partnership, including the name and Federal Employer Identification Number (FEIN) at the top of the schedule.

- Partner Details: A complete list of all partners, including their names, addresses, social security numbers (SSNs) or FEINs, type of entity, and ownership percentage, must be provided in columns 1 through 4 for each partner.

- Nonresident Partner Reporting: Special attention is required for nonresident individual partners. Columns 6 through 8 are specifically designed for reporting income, tax withheld, and other pertinent details for these partners.

- Income and Loss Reporting: The form mandates reporting the federal distributive share of income or loss for all partners in Column 5, ensuring that the partnership's income is allocated correctly among its members.

- North Dakota Tax Withholding: For nonresident individual partners, the North Dakota distributive share of income and the North Dakota income tax withheld at a rate of 4.86% must be reported in Columns 6 and 7, respectively.

- Documentation and Attachments: If the space provided on the form is insufficient, additional pages can be attached to include the necessary details for all partners. This ensures that every partner is accounted for and their information is fully documented.

Accurate completion of the North Dakota 58 form is essential for partnerships to comply with state tax regulations. It not only facilitates the proper reporting of income and deductions but also ensures that the tax responsibilities of both resident and nonresident partners are met. Reviewing the instructions provided on page 7 can further assist in filling out the form correctly and avoiding potential errors.

Browse Popular Documents

North Dakota Nonresident Filing Requirements - Emphasizes the significance of attaching a complete copy of the 2009 Form 1041, including Federal Schedule K-1s, for comprehensive filing.

Sfn 12011 - Aims to streamline state oversight of the construction industry by standardizing the renewal process, making it straightforward and comprehensive.

North Dakota Filing Requirements - Instructions for annual filers on Form 306 simplify the process for businesses that prefer or qualify to submit their withholding information once a year.